What a year! 2020 has definitely shaped up to be a year that I don’t think any of us will forget anytime soon. From surviving lockdowns to an economic recession and the crazy gains in the stock market, there has indeed been some very crazy moments this year and I thought I’d take this time to do a year-end review as I always have.

Sharp-eyed readers may have realised that I forgot to do a 2019 savings reflection – my bad! I didn’t even realise I had missed it out because I was too busy adapting to my new role as a first-time parent.

But before that, here’s a quick recap of previous years:

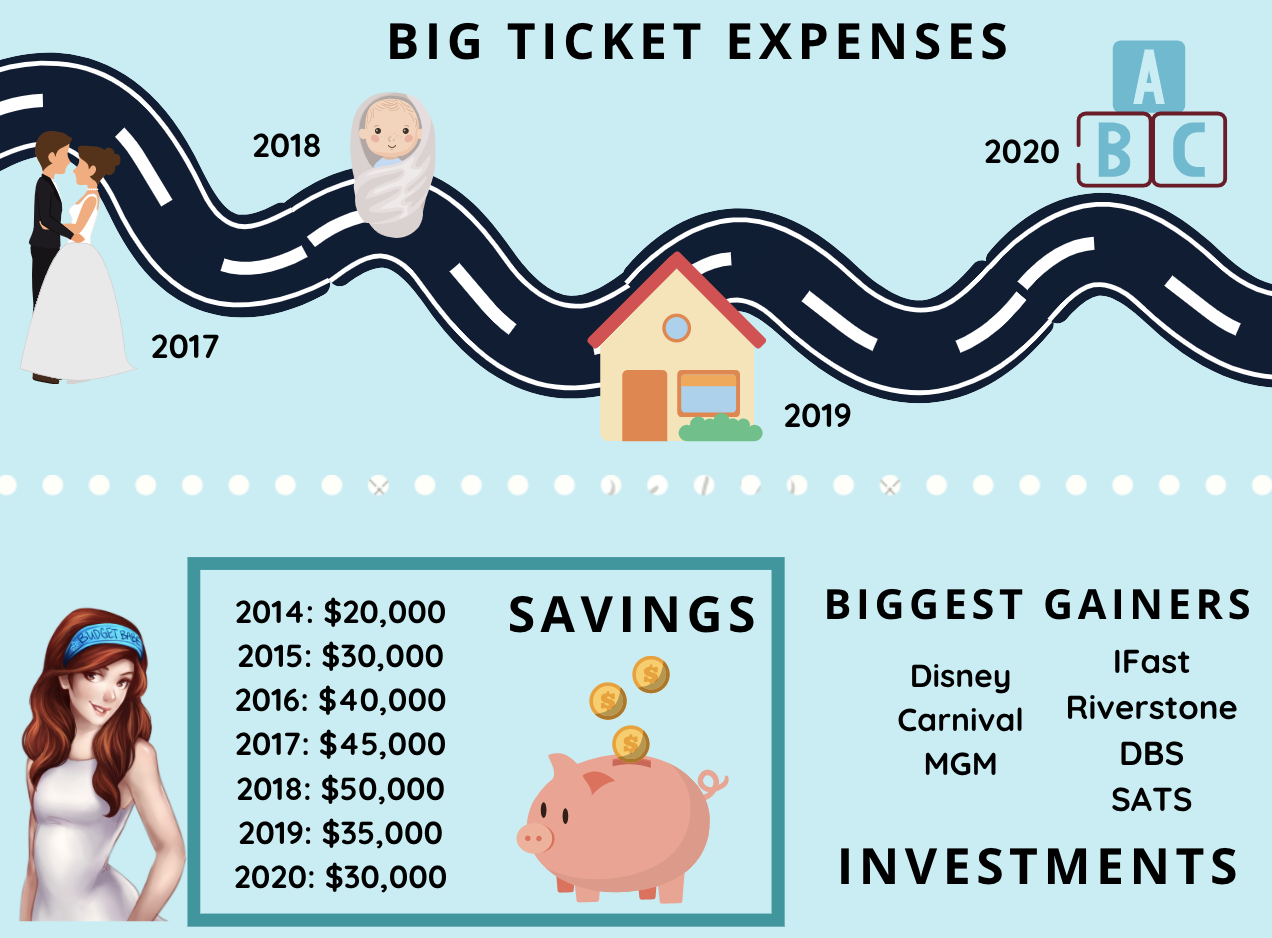

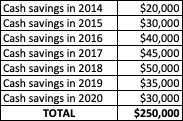

- 2014: Saved $20,000

- 2015: Saved $30,000 and grew income

- 2016: Saved $40,000 and grew income, hit $100k in net worth at age 26 including CPF

- 2017: Saved $45,000 and doubled my net worth in a year

- 2018: Saved $50,000

- 2019: Saved $35,000 (didn’t realise I completely missed out on a round-up post, but here’s our child-related expenses instead)

Savings

Much of this cash is now sitting in my investment portfolio or our emergency savings fund, if you’ve been paying attention over the years, you would have realised that my savings have actually trended downwards – especially with the following big-ticket milestones:

- 2017: Wedding

- 2018: Pregnancy + Nate’s birth

- 2019: House downpayment

- 2020: Renovation + Nate’s education

With saving money being so ingrained in my nature, it has become easier to save more money with lesser effort as I grew older.

Older and wiser now, my financial goals have changed significantly in recent years. Prior to marriage and parenthood, I focused largely on increasing my savings, growing my side hustles and maximising rewards on my expenses.

However, sandwiched between a young toddler and our ageing parents today, my priorities have now shifted towards greater protection and ramping up our investments.

Income vs. Expenses

It has truly shown me the importance of building up passive income instead of hustling so hard for active income, because there’ll come a time when you burn out.

As much as I wish to increase my income over time, I didn’t receive a pay raise (again) this year at my corporate job. In fact, the oddest thing happened because I had initially tendered in December (remember my announcement here?) but got called back only to see my (higher-paid) colleague in my team get retrenched.

Given how the lockdowns were affecting my husband’s income at that time, I decided to play safe and head back, but never expected the heavy workload that was about to come my way, especially as I had to cover for my (retrenched) colleague and also my European teammate who went on an extended maternity leave. In all honesty, having stuck around for so long and not receiving a pay increase (despite asking every year) for the past 4 years is really making me rethink my career options. I used to think that loyalty would pay off, but after 6 years at the same place and seeing how the new blood are always paid higher, it is time I acknowledge that loyalty does not pay in the corporate world when it comes to your salary.

If a better opportunity comes along, I won’t say no this time.

Insurance

With more dependents (and ageing parents), our insurance costs have definitely gone up significantly as we added on more plans to “stack” our coverage. As much as I’d love to reduce our insurance costs further, there are some things in life that we simply cannot skimp on, given that the risks of being uninsured (or under-insured) in our case would be too high as our income goes towards supporting so many people.

We’ve tried to keep this as low as we could by opting for term over whole life plans, and stacked critical illness coverage.

Investments

2020 has been a crazy year in the stock markets, and my overall investment portfolio has done better than what I expected, at about ~40% to 70%!

Much of these gains were from my bulk purchases in March, and skewed by the gains in my largest position (Disney) which is up almost 100%. Locally, my positions in iFast and Riverstone (all accumulated prior to the pandemic) performed exceedingly well beyond >200% (Riverstone was almost 4x at one point, but I didn’t sell), as well as my recovery plays in DBS and SATS, have also done well at 30% to 50%.

As readers would remember from my previous webinars, I also made the move to go heavily into U.S. technology stocks during the lockdowns, which has served me well given that most of my positions in this sector are now sitting on 20% to 80% gains in just the last few months.

This is the first time in my investing journey that I’ve seen such crazy gains, and I’m not expecting the same volatility to repeat in the coming years.

Reflections on 2020’s finances

1. Being too conservative with cash.

2. The need to grow my income further.

3. Fix the “leaky buckets” to save more in future years.

6 comments

Congrats on your financial goals! 2020 has indeed been a rough one and tested investors conviction during the sharp decline. Thanks for documenting your journey and inspiring me to start my own too! Have a great year ahead!!

Cheers,

KO

My advise is keep credit cards that you use frequently. I used to have many cards by thinking of utilizing the unique benefits of each card but end up loss track like you. Now I only keep 4 cards which each card I use for different category of expenses.

Disagree with your reflection on setting aside 24 months emergency savings is not a wise move because you based on worst case didn't materialize. Emergency savings by definition is meant for emergency spending, so you shouldn't discredit it when such spending didn't happen.

If staying invested means investing in stocks, then when the needs arise, you may be liquidating your stocks at a loss amidst bear market. Imagine when you need money during March crash without any emergency savings.

What you can do is to park emergency savings into instruments that are capital guaranteed, yield better returns than bank deposit and liquid enough to withdraw as and when needed. Example is insurance savings plans with no lock-in period for withdrawal.

Haha it was a move that turned out (on hindsight) not to have been wise, given the market's huge rise, but definitely a move that I would have made again with no knowledge of the future.

Our emergency cash is already parked in those instruments 🙂 I've reviewed some of those tools over here on the blog in the past few years!

Definitely! I've trimmed down the number of credit cards we own already. My top pick for just ONE is still DBS Live Fresh, given our nature of spending.

Haiya, when young with lots of energy, easy to track. With a kid and suddenly so many other things to look after…not so easy anymore. Lol.

I'm sure you'll do as well, if not better! 🙂 Jiayou!!

Comments are closed.