|

| Image credits |

How many times have you sought advice from a “financial advisor” (i.e. mostly a glorified term for an insurance salesperson), only to be left sorely disappointed when they end up selling you insurance products (usually expensive / high commission plans)? You’ll hardly find agents who tell you about “no commission” products that are actually great for various needs (eg. CPF-SA, Singapore Saving Bonds, Temasek Bonds, Astrea IV bonds, etc).

And so you try to DIY your own insurance through portals like CompareFirst, but you’re also stuck because you cannot figure out if you’re identifying your own insurance protection gaps correctly. As a result, you either end up under-insured (from DIY-ing wrongly), over-insured (if you listen to your insurance salesperson), or even worse, not getting insured at all (!!!!).

To try and address this problem, a joint venture was set up between NTUC Enterprise Co-operative and Providend Holding (which owns DIYInsurance). Their aim is to reach out to individuals and families who need to save and invest, but are currently being under-served by banks and financial advisers.

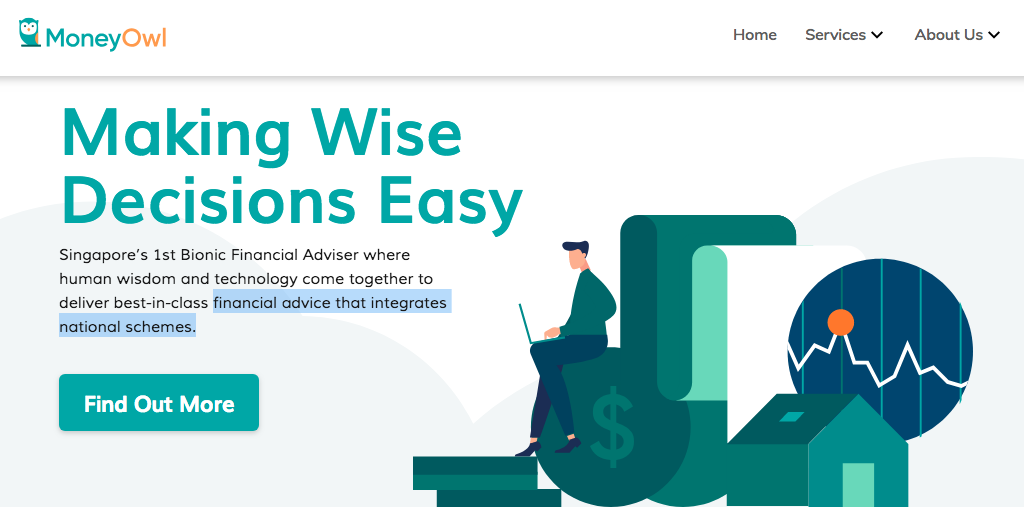

The result is MoneyOwl, which purports to be Singapore’s first bionic financial adviser – where human wisdom and technology come together to deliver financial advice that integrates national schemes (like CPF, MediShield, ElderShield, etc).

MoneyOwl recently approached me to try out and review their platform, so here’s what I think:

1. Suitable for both the clueless and the savvy insurance consumer.

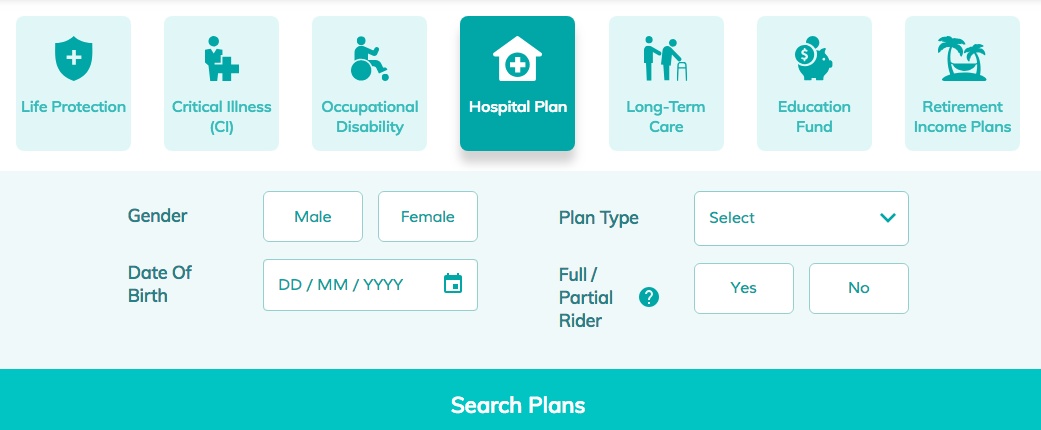

Click on Find Out What I Need to fill in your profile and get a preliminary analysis from their AI robot technology, which employs an algorithm to identify your protection needs and provides recommendations on what type of insurance products you might want to look at getting (as well as giving you the top 2 cheapest quotes).

If you already know your own insurance gaps and you’re just looking to compare quotes, you can click on I Know What I Need to get started. That will bring you to this page:

Previously, consumers could compare on either DIYInsurance or CompareFirst (by MAS), but both portals were lacking in many areas such as having limited insurance products and a cap on coverage. If you wanted or needed anything else or higher, you would still have to go through an insurance agent to get the quote. I’ve reviewed both platforms previously here as well.

And if you need to speak with a human for a second opinion or to ask more questions about the recommendations provided to you, you can opt to be contacted via phone, email, web chats or even meet up face-to-face with MoneyOwl’s team of licensed advisers.

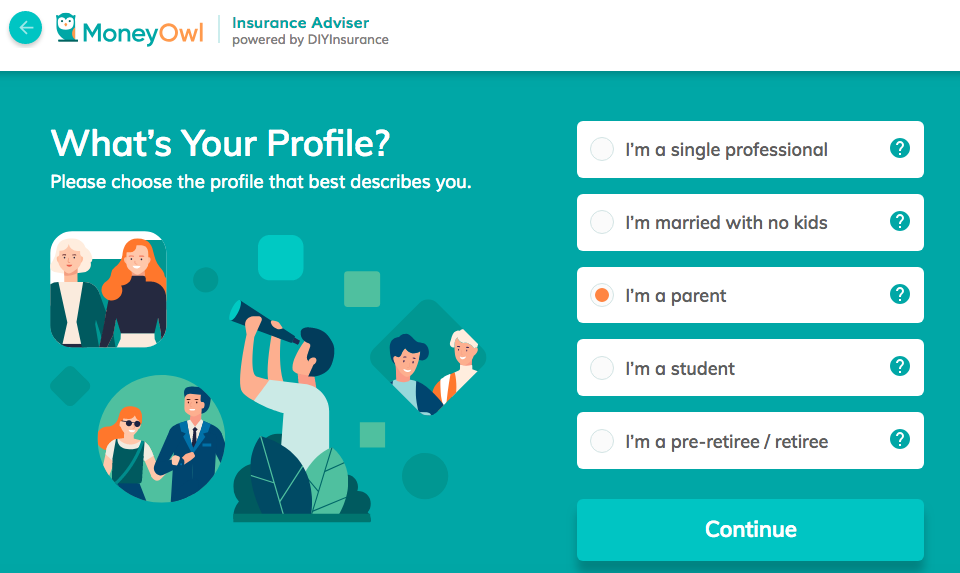

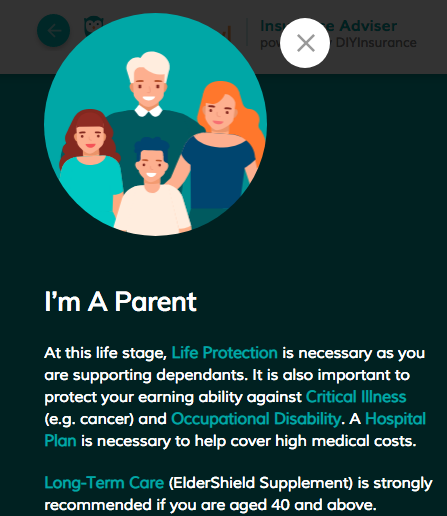

2. Your insurance needs are sorted by your profile and life stage.

This is even better than DIYInsurance’s previous Self Check tool, which I reviewed here and provided recommendations on what needed improving on.

|

| As most of you would know by now, I’ve hit 9 months of pregnancy and my baby is due to be born anytime now, so I tried out this tool using my new status as a parent. |

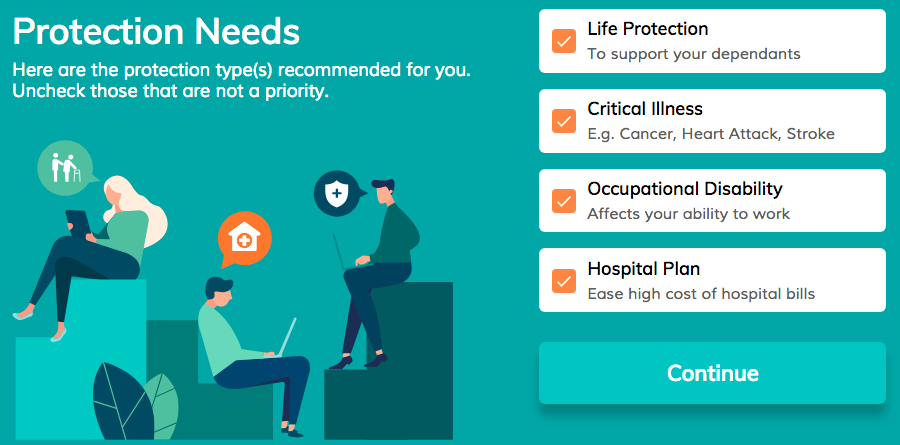

3. Your protection needs are determined by your life stage and number of dependents.

Regular readers will know that I’m in a tight spot because my husband and I have a pretty high number of dependents to look after – 5, to be exact – and we’re alone in this. That number will probably grow to 6 soon because we’re hoping to have a second child in the near future as well.

As a result, we cannot afford to just save and invest – we need to turn to insurance to help mitigate the larger (potential) bills in the event of any unfortunate incident as well, otherwise a single large bill for either one of our dependents could very quickly wipe out our entire cash savings and assets.

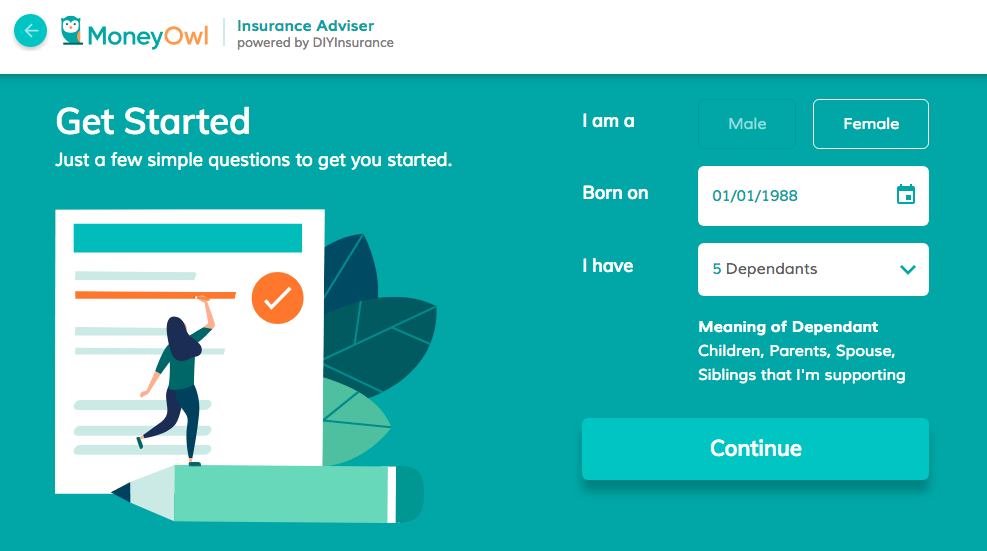

4. You can fill up your profile, and it is pretty non-intrusive.

Don’t you hate it when companies ask for private and intrusive personal information like your name and contact number before they reveal a quote / other information to you? You just know that they’re using it as a tool to follow up later and sell you something!

If you’re such a consumer like me, then you’ll appreciate how MoneyOwl doesn’t require you to furnish them with personal identifiable details like your name or contact number. As long as you wish not to be contacted, you have the option to go through the entire process, get the recommendations and quote, and get out without worrying about a pesky salesperson calling you afterward.

But at the same time, if you do wish to be contacted and speak to an advisor for more details beyond what the tool is recommending you, MoneyOwl also allows you to create your profile and leave your email address so they can get in touch with you to either discuss further.

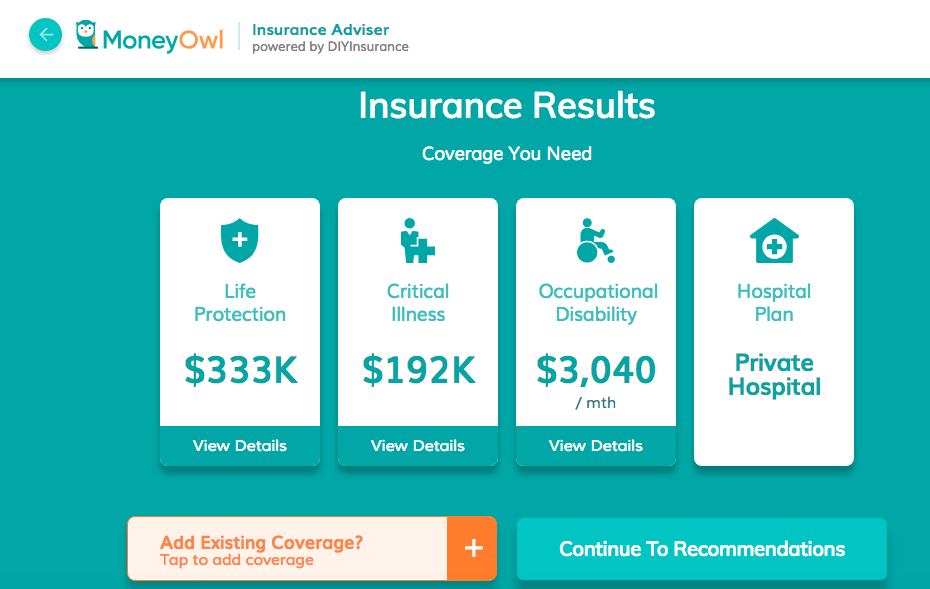

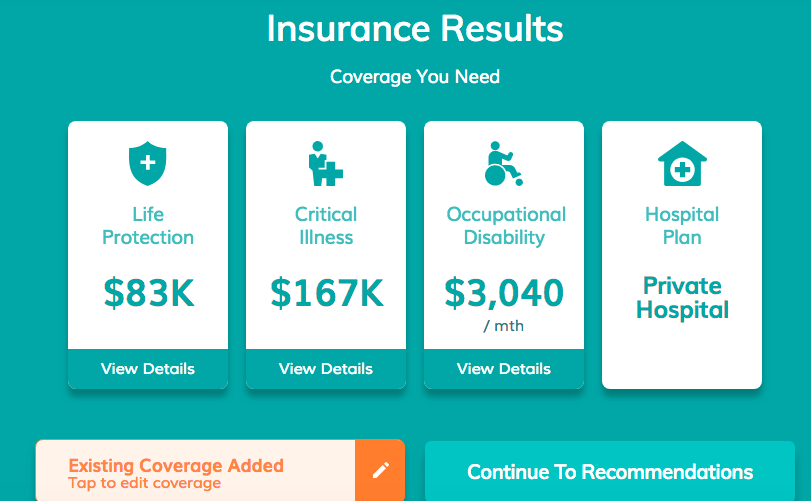

5. It not only identifies your insurance needs, but also allows you to add your existing coverage so that you can get an accurate assessment of what your remaining gaps are.

This was the coverage suggested for me:

And this is what I got after adding my existing insurance coverage:

The recommendations then showed me a few low-cost options which were ranked by the cheapest premiums. You also have the freedom to choose to buy through them, or through other means (eg. direct or through your own agent). If you buy through MoneyOwl, you get back 50% of agent’s commission rebate (the remaining 50% goes towards the company’s operational expenses and investing in R&D for the other modules).

My thoughts?

This is great and a huge game-changer for the insurance industry. I love the idea, the interface, and the fact that there’s the option for consumers to speak with an adviser if they need additional support. After all, I still maintain that technology can never fully replace the empathy and emotional concerns that only a human adviser can relate to.

Of course, I’ll be lying if I said their platform is PERFECT – there will always be room for upgrading, and I’ve since provided my list of recommendations for them in terms of (mostly minor) improvements they can work on. For instance, I spoke with their Chief Advisory Officer to ask if they would still recommend a term policy for someone who wants cash value back for all that premiums paid; the answer was that they will then educate the client on the difference between using term and whole life plans, but recommend whole life only if certain conditions are met. I like that, because whole life isn’t necessarily a bad product per se (although it certainly does lose out to the buy-term-invest-the-rest approach most of the time).

Another point of contention I brought up was that ranking hospital plans by cheapest premiums isn’t necessarily a good way because the cheapest for this particular type of policy does not always mean the best value-for-money. AIA hospitalisation plans, for instance, may be more expensive than NTUC Income, but that’s because the pre and post-hospitalisation coverage that they offer are a lot more as well. MoneyOwl then told me this is where the client assessment with their human advisers will come into play.

|

| Source: The Straits Times |

Aside from insurance, you can see from MoneyOwl’s website that they will soon roll out a digital will-writing service, an investment portfolio featuring low-cost funds, and a comprehensive financial planning service that will integrate national schemes like CPF and ElderShield. I’m excited to see these new roll-outs in the near future.

As most of you know, the biggest problem in the insurance industry is that there is little incentive for agents to recommend products with zero or low commission rates.

And is that really surprising, when agents rely on these commissions to earn a living? It is a well-known fact that commissions are fiercely guarded by the insurance industry – remember how in 2013 when 10 financial advisory firms pressured iFast Financial to withdraw insurance products from its Fundsupermart website which would have offered a 50% commission rebate to consumers?

As long as commissions continue to be tagged to agent recommendations, unbiased advice is but an idealistic dream that is mostly impractical in reality.

|

| Source: The Business Times |

1 comment

Nice Fantastic information !!! I'll be enchanted to greatly help due to what I've learns from here.I like the quality of your blog.

SGX stock Advisory

Comments are closed.