Astrea IV Class A-1 bonds are the talk of the town right now, and I’ve received so many DMs about this so I’m finally sitting down to evaluate and write this.

Details:

– The bond is launched by Astrea IV Pte. Ltd, which is an indirect subsidiary of Temasek

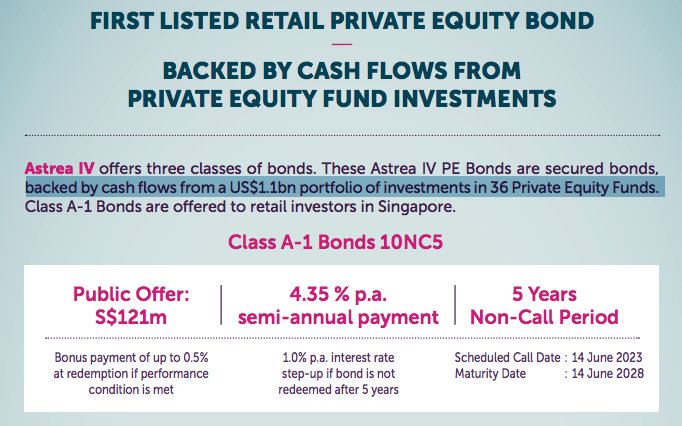

– 4.35% interest rate offered

– IPO applications close at 12 noon on 12 June 2018

– You can apply through ATM or online banking via DBS, POSB, OCBC or UOB

– Minimum subscription amount: S$2,000

– You CANNOT use your CPF or SRS funds to apply for this bond.

– Bond starts trading on SGX-ST on 18 June 2018

What are you really buying into?

Now, don’t get misled by the above headline published in The Business Times last week – this is NOT a Temasek bond. Rather, it is a bond issued by one of their subsidiaries.

This is a really new and unique asset class because they’re neither government-backed nor corporate bonds. Instead, they’re private equity bonds. This is the 4th private equity bond that is being issued by Astrea, and the first one that is being opened up to retail investors.

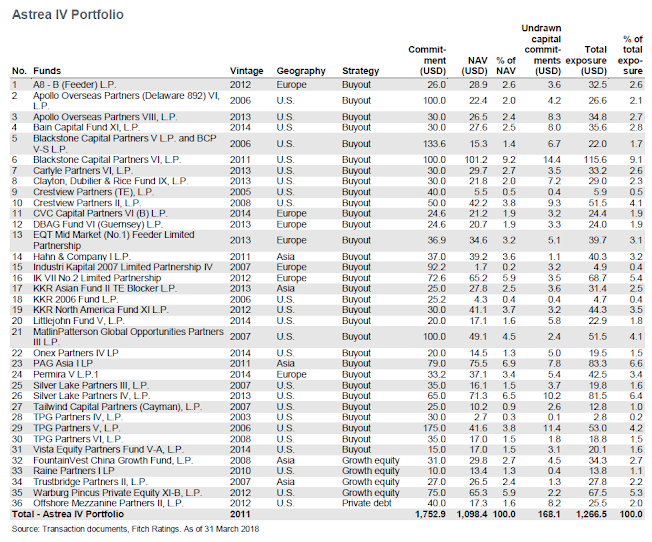

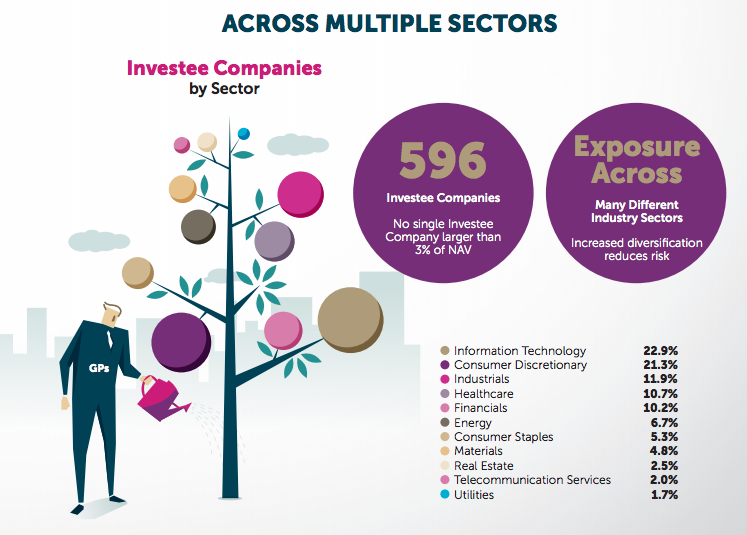

These Astrea IV Class A-1 bonds (“Astrea bonds”) will then be used to invest across 36 private equity funds, which are invested into 596 underlying companies. Traditionally, I would dig up details about the investment assets, but since there’s 36 funds and almost 600 companies, that’s an almost impossible task because much information isn’t available about these private companies, and neither does anyone have that much time anyway to scour through all.

|

| The 36 PE funds. |

If you’re unfamiliar with private equity, what they basically do is to invest in distressed or promising companies, go in with their expertise and restructure or turn the business around (usually making operational or financial improvements), with the final aim (usually) being to sell it off for a profit. As a result, the returns on such investments (when successful) can be tremendous – think 2 to 3 digit percentage figures at least.

So in this case, when you buy these Astrea bonds, you’re pooling your cash which will then be used to invest into these funds and underlying companies. The profits will then be used to pay the interest on your bond (4.35%) and finally return you your capital after 5 years.

Given the sheer number of funds and underlying companies, coupled with the fact that the exposure to a single partner / company / sector is quite low (even Blackstone Capital Partners, which is the largest, is merely 10.6% of NAV), the risk here is quite minimal even if one or some fold.

(There’s a step-up interest portion in these Astrea IV bonds if they’re not reclaimed after 5 years i.e. on 14 June 2023, but I’m not going to go into that because I’ve no intention to hold it for any longer than that, due largely to opportunity cost. There may be a bonus payment of up to 0.5% at redemption if performance condition is met.

For those of you who are keen on a longer-time holding period, there will be a 1% per year interest step-up rate if the bond is not yet redeemed after 2023.)

Who’s behind the bond?

Okay, so now that you know this is NOT a Temasek bond…then who exactly is behind it? That’s Azalea Investment Management, which was set up in 2016 and is a wholly-owned subsidiary of Azalea Asset Management, which is then owned by Temasek Holdings.

Although they’re relatively new as an entity, Azalea’s management team apparently has extensive experience and institutional knowledge in the private equity space. The senior management team comprises of PE veterans and is led by Ms. Margaret Lui-Chan, who has been with Temasek since 1985.

Temasek and its affiliates have also launched 3 Astrea investment vehicles prior to this.

Check out this really informative Fitch report for more information.

Why is the yield so high?

That was the first question that came to my mind when I read about the bonds being launched. Compare this to the Singapore Savings Bonds which is pretty much 100% risk-free (since it is backed by the Singapore government) and yields 2.63% for this month’s issuance. Now contrast this to a riskier corporate bond such as Aspial’s bonds, which were launched for 5.25% previously.

If this is from (albeit indirectly) Temasek, the next financial juggernaut in Singapore, then why is the yield so high?! Wouldn’t it make more sense to price it at about 3+% yield, since the brand name Temasek alone would warrant some sort of a premium and perceived safety net?

According to Ho Ching, she says the main aim of this bond is largely to help retail investors in Singapore supplement their retirement income.

Why is the yield so low?

You didn’t read that wrong 😛 for investors who truly understand the huge kind of returns that are seen in private equity (remember, 2 or even 3 percentage digits can be fairly common, if they spot the right gems / get lucky on the sale), why is the yield being offered to A1 bondholders here so low at just 4.35%?

This can be easily explained using high risk, high returns; low risk, low returns.

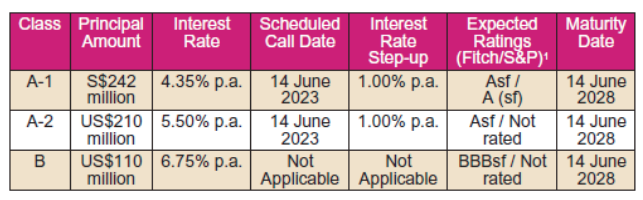

Firstly, the minimum investment amount to participate in Class A-1 bonds is just S$2,000, in contrast to Class A-2 and B (US$ 200k each).

The risks in Astrea IV Class A-1 bonds in terms of default are also significantly lower than the other bonds issued in this exercise, as Class A-1 bonds will be redeemed first in any event before A-2 or B. This means that even if Astrea faces liquidity or financial problems, A-1 bondholders will be paid first.

Since the risk undertaken by class A-2 and B bondholders are higher (they only get paid after A-1), they’re compensated with a higher yield in order to incentivise them to buy these bonds. Unfortunately, you don’t get to buy them as they’re not open to the public and have already been fully subscribed anyway.

Are my returns guaranteed?

No. You MUST understand this point.

However, the risk of default is pretty low, in my opinion, due to how this has been structured. In the event of a shortfall, Astrea IV also has a 10-year committed capital call facility with DBS which will step in to cover the payments 🙂

When can I get back my money?

You can sell the bonds anytime after 18 June 2018 on SGX, just like how you would with ordinary stocks. Otherwise, you can also choose to hold the bonds until its call date on 14 June 2023, or even longer if you want to be entitled to the step-up interest (provided the bonds aren’t fully redeemed by then).

Is there a chance that I’ll lose my money? Will Temasek save us if anything happens to Astrea?

The direct risks to bondholders which you should be aware of are:

– the bond price might fall below its issued price on the bond market

– the Manager might not be able to fulfil its interest repayments

– the Manager might not be able to reclaim the bonds and pay back the original capital sum to bondholders

Now, it is important to note that Temasek Holdings is not guaranteeing these bonds. This is even explicitly mentioned in the prospectus, that is, if you bothered to read through (all 306 pages of) it. Therefore, if the bond manager fails to repay the bonds and/or interest, there is no guarantee that Temasek will step in to save bondholders.

Are they capable of repaying the bond interest and capital?

As with all bonds, you should always evaluate the financial health of the investment manager before you decide whether to buy or stay out. Remember, that’s the main reason why I said I was staying away from Aspial and Hyflux bonds back then?

Since Astrea’s financials are not entirely public and we can only rely on the numbers presented in their prospectus covering a limited timeframe of August 2017 – March 2018, a few figures to highlight are:

– USD 48.6 million of profits generated

– USD 342.5 million was used for their investing activities

That doesn’t really tell us much, especially when there’s no year-on-year comparison to gauge how they’ve fared. Therefore, we can only look to their Loan-to-Value below, where you’ll see that Class A-1 bonds have a LTV of 16.5%, which is relatively low, and thus the chances of default should also be quite low since only $181 million in the reserve account is needed to fully redeem Class A-1 bonds.

Sounds good, but what’s the catch?!

I’m a huge skeptic, so this deal honestly sounded too good to be true to me. But after scouring through the prospectus and various bloggers / investment houses’ take on this bond IPO, I struggle to find anything realllllly negative about it.

Initially, I thought, is this some conspiracy?! Why would Temasek issue a bond with such a high yield?! Can’t they get institutional or corporate loans for this? I bet companies would be scrambling just to subscribe! Or just get the private banks to issue it to their high-net-worth customers? Then I thought, or maybe they’re in financial trouble, that’s why they’re raising this money from us mortals? But then I realised that the total sum of S$242 million raised really doesn’t count for much, considering Astrea’s access and connections to Temasek Holdings.

My cousin attended the talk on this bond yesterday and I got her to ask them this question on my behalf. The answer by their CEO, Ms. Margaret Lui-Chan was that their vision is to open to retail investors. Lol.

So I can only say, looks like Ho Ching might be right after all, and this bond truly is being created to help retail investors? You can be the judge.

Disclaimer: I am NOT sponsored, nor do I have any connections nor payment from Temasek or Astrea or anyone, for that matter, in exchange for this post.

TLDR Summary

This is probably the longest IPO analysis I’ve ever written for a single product, so if you got bored halfway, I don’t blame you. Here’s a quick breakdown of my view towards Astrea IV Class A-1 Bonds:

Pros

– This is one of the safest bonds I’ve seen in a long time, especially given the A-rating by two reputable rating agencies (Fitch and S&P), not to mention Ho Ching putting her own personal name behind this (I assume, since she didn’t correct the BT article nor ask them to apologise / correct / take it down).

– Long track record since this is already the 4th Astrea bond being launched, with the first in 2006.

– There are some quality PE managers in the 36 funds listed above, including Blackstone and KKR. Private equity folks should recognise these names 😉

– The Sponsor owns 55% equity interest, so they do have their skin in the game and are less likely to want to see this fail.

– Their marketing is rock solid and has definitely generated the hype needed for this to become over-subscribed. Talk about FOMO!

– The first few pages of their IPO prospectus is just lovely! Kudos to whoever designed it 😀

Cons

– It is not easy to understand, and is the first of its kind for retail investors.

– It was slightly mis-marketed (in my opinion) since there was so much emphasis and hype on their connections to Temasek, leading many investors to think this is essentially a Temasek Holdings bond.

You can also watch this short (marketing) video explaining the bonds here:

So Budget Babe, are you subscribing?!

Considering the hype and 4.35% yield, I’ll be subscribing to these bonds and leave it as part of my bond portfolio (together with my CPF). After all, I’m the biggest skeptic of most corporate bonds, but this is one in recent years that actually managed to get my attention.

With their connection to Temasek, I doubt that Astrea will default on the bond interest payments, and I don’t think their bond prices will fluctuate too much on the open market either.

But please don’t follow me – do your own homework! Here’s the full 306-pages of the bond IPO prospectus as well as the Fitch report for you to read before you make your next move. Nonetheless, I’m betting this is going to be oversubscribed, and can only hope that I get some allocation from my application!

December 2023 Update: My Astrea Class A-1 Bonds have been redeemed on its Scheduled Call Date! Hooray! Now on to redeploy the capital elsewhere 🙂

With love,

Dawn

16 comments

Thanks for the write-up Dawn! Have been reading some conflicting literature on the topic, but what are your thoughts on the impact of rising interest rates on these bonds?

Pretty informative analysis. For one thing didn't know that it is owned by a subsidiary.

thanks for the detailed analysis! I tried finding out opinions from many "experts" on hwz forums and the consensus there is generally negative. Given my limited investing knowledge and the risk-vs-returns of this product, I might honestly give this a try.

Thanks for the detailed and clear write-up. As i am quite new in investing, just want to check on the interest rate pf 4.5%. Is the interest returns based on annually or after the maturity period? Supposedly i invest $4k, i will get back $180 (interest) and $4k (capital) after 10 years?

Regards,

Noob beginner

This comment has been removed by the author.

The 4.35% per annum is calculated every year you hold the bond, but broken into 2 payments to be paid out every 6 months. For a principal investment of S$10k, 4.35% pa means S$435. your bank account (which is linked to CDP) will see S$435/2 or S$217.50 credited every 6 months.

This comment has been removed by the author.

valid concern! but given their loan structures, I'm not worried TOO much (but will definitely continue to keep an eye on it!)

ikr…the way it was marketed was a tad misleading on the national papers, if I might say so myself.

haha I realised lots of the negative comments came from anti-PAP / anti-govt folks as well, so it's always good to read their concerns while checking whether their opinions are valid, or if we're looking at the same thing and holding different opinions 🙂 no right or wrong here!

As answered by Rachel! 🙂 it's also in the prospectus 🙂

a lot of "experts" also say things like "I can easily do X and Y in my portfolio, also can get better returns than 4.35%". What's your take on this kind of opinions? You seem pretty savvy yourself, and having seen a few of your other investment-related posts, I think 4.35% is peanuts to you (no offence meant) haha

how do we get notified on these IPOs?

Read the news, or check SGX

it is all about portfolio management – I have a portion of my portfolio allocation to risk-free or low-risk assets / dividend plays, undervalued counters, growth stocks, and then high-risk investments.

given my age and longer investing timeframe, my low risk investments are almost nothing – save for my CPF. I've been waiting for the longest time to add a corporate bond into that segment of the portfolio, but as you've seen from my previous articles on corporate bonds that have been launched over the last few years…nothing really excites me or makes me confident enough to park my money with them.

obviously the amount I put in this is nothing compared to the amount I put into a single undervalued counter, as the undervalued component of my portfolio yields me much higher gains (typically double digits in capital gains) and obviously outperforms these Astrea bond payouts. but to put ALL my eggs into one basket would be quite silly / risky too, wouldn't it? haha

so since I need something to add to my low-risk segment, and Astrea looks to be the best option in 2 years that I've seen so far, I've put in a small allocation.

how small or how much? that's a secret, but if it helps, I got 100% of my allocation. if you read the news, you should know the range that falls under 😉

off-tangent observation: a lot of people like to talk about their "expertly allocated" portfolios, but at the same time all are so secretive about it. what do you stand to lose if, say, I were to copy your entire portfolio? after all, the purpose of your blog is to help your readers towards financial freedom isn't it? apologies for the offensive tone; it's not meant to criticise or shoot you in anyway, but just something i'm curious about. clearly i don't understand much about the art of investing.

Comments are closed.