Some of you might recall my controversial post several years ago when I mentioned I didn’t have any intention of using my CPF to pay for housing, and prefer to use cash instead for repaying a bank loan at 1+% interest rate per annum. Our reasoning was to let our CPF grow instead, since 2.5% p.a. is still a decent rate.

I thought I’d do an update because as it turned out, we didn’t end up utilizing that strategy in the end. That’s because when we moved into our house in 2020 at the start of the pandemic, it was also the time when global stock markets crashed. Being opportunistic, my husband and I decided to inject our cash into the markets (instead of financing our mortgage) and use my CPF to pay for the monthly mortgage in the meantime.

While some of my peers chose to utilize their emergency savings, or even make use of balance transfers during this time, we saw our method as a way to “borrow” from our (future) selves to capitalize on the current market opportunities. This way, instead of having a bank earn our interest, it would be ourselves earning it.

The idea was then to do a Voluntary Housing Refund to “repay” ourselves thereafter when there are less investment opportunities (or when the outlook isn’t as obvious / easy to invest).

Well, this turned out to be the right move, as our investments that year did well as the markets recovered.

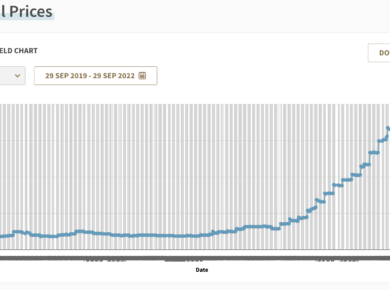

Based on CPF’s latest statistics, we aren’t the only ones who are using our CPF for housing:

Of course, if you lack liquid cash to put back into your CPF or aren’t keen on a Voluntary Housing Refund (for whatever reason), you can also refund your CPF accrued interest upon sale of your property.

This was what happened to my parents after they sold their flat, although financing the mortgage with their CPF over the years had led to a substantial sum of accrued interest, leaving them with less cash proceeds than if they had used cash (or partial cash, or did a voluntary refund).

But if your sales proceeds from your property aren’t enough to repay the accrued interest, there is no need to top up with cash. Until today, I’m still seeing this myth going around, so please take note.

And if your elderly parents have a HDB flat, you can also talk to them about whether the Lease Buyback Scheme and Silver Housing Bonus as an option for their retirement. You can read about them here:

- Sell part of your flat’s lease to HDB to monetize and receive a stream of income for retirement

- Check your eligibility for the Silver Housing Bonus when you downgrade your property

More seniors are taking this up, and if you asked me, the best part about this method is that they cannot be scammed of this lump sum of money so that they continue to receive monthly payouts to finance their retirement years.

Should you use cash or your CPF to pay for your mortgage? That is completely up to you, and I hope that by doing this update, you can see from both perspectives.

Should you do a Voluntary Housing Refund? If you want to stop the accrued interest payable from growing, and let the government pay you the interest on your savings instead, then that could be a good option to consider. Of course, this option may not be available to those who lack sufficient liquid cash on hand.

And as for your parents, if you’re worried about their retirement and don’t need them to leave you their HDB as an inheritance, then the Lease Buyback Scheme and Silver Housing Bonus could just work in your favour (note: Singaporeans cannot own two HDBs. If you currently own one and inherit your parents’ flat later on, you will need to sell one).

With love,

Budget Babe