Applications for the Lendlease Global Commercial REIT IPO opens in just 2 more days.

This is probably the most exciting IPO I’ve seen this year, and I was gearing up for the release of its details ever since the news first broke in May that Lendlease was planning a listing on SGX.

My son just fell asleep, so I’ll keep this short and cover only the main points within my investment thesis.

Details

– 387 million shares are being offered to the public at S$0.88 each

– IPO opens 25 September at 9 pm

– Deadline to apply is by 12 noon on 30 September

The business

The Sponsor’s name should be a familiar one to most Singaporeans, since Lendlease is behind several much-loved shopping malls – JEM, Parkway Parade, Somerset 313 and the latest Paya Lebar Quarter.

As one of the largest developers in the world, the Lendlease Group has close to AUD$100 billion in development assets globally. Its 60-year-old history has seen it develop some of its hallmark projects including Paya Lebar Quarter (Singapore), The Exchange TRX (Kuala Lumpur), Barangaroo South (one of the most significant waterfront transformations in Sydney) and of course, its recent residential project in conjunction with Google to deliver over 15,000 new homes in the San Francisco Bay Area.

As Lendlease Global REIT aims to provide a mix of retail and office, 2 properties have been selected for injection into this REIT at the moment:

- 313 Somerset

- Sky Complex (3 office buildings in Milan)

It is disappointing that they have only selected 2 properties to be part of the investment listing portfolio, but not difficult to see why, as both combined provide the REIT with an extremely high occupancy rate and a diversified tenant base. While I was hoping for Paya Lebar Quarter to be included as part of its Singapore exposure, I can understand why they didn’t – the mall has yet to pick up momentum and its numbers would probably pull down the rest.

Since the REIT has the right of first refusal to its Sponsor’s portfolio, I’m hoping that the Sponsor will inject more assets in the next few years, given the huge pipeline of assets that are ripe for the picking.

The numbers

- A fairly healthy WALE of 4.9 years, but only because it has been pulled up by Sky Italia’s office lease in Milan despite the short WALE of Somerset 313 tenants

- High occupancy rate of at least 99.0% since 2016. (For those of you scratching your head over the combination of the 2 selected properties, this should give you a big clue because it makes their numbers look exceedingly attractive.)

- The Lendlease Group will hold about 24% – 27% of the REIT post-listing, which aligns their interest to grow the REIT’s net asset value and distributions per unit over time.

- Price-to-book (P/B) ratio of 1.08

- 5.8% – 6% indicative dividend yield. Not too fantastic, but nothing too shabby either.

Also note that 5% per annum of the REIT’s Net Property Income (NPI) will contribute to the Management’s performance fee, which will be paid in the form of units together with the base fee for 2020-2021. This is good news as there will be vested interest for the Manager to ensure NPI growth for the REIT.

A strong list of cornerstone investors

It has been a longgggggg time since I’ve seen such a power-packed list of cornerstone investors, namely:

- AEW Asia Pte Ltd

- Asdew Acquisitions Pte Ltd (aka Wang Yu Huei’s investment company)

- BlackRock Inc

- DBS Bank (on behalf of their wealth management clients)

- DBS Vickers Securities (on behalf of their corporate clients)

- Fullerton Fund Management

- Lion Global Investors

- Moon Capital Management

- Nikko Asset Management Asia

- Principal Asset Management (a joint venture arm with CIMB Group)

- Soon Lee Land (public housing and condo developer in Singapore)

- The Segantii Asia Pacific Equity Multi Strategy Fund

- TMB Asset Management (recently acquired by Prudential)

Those of you familiar with the investment world of Who’s Who should recognise many of these names. It makes me wonder if there’s some information the big boys have about this REIT IPO that the rest of us might not be privy to.

S$399 million of units have already been taken up by the cornerstone investors. My only concern is that these cornerstone investors are not subject to any lock-up restrictions in respect of their units, which means whether or not they’ll sell on opening day is anyone’s guess.

Opportunities

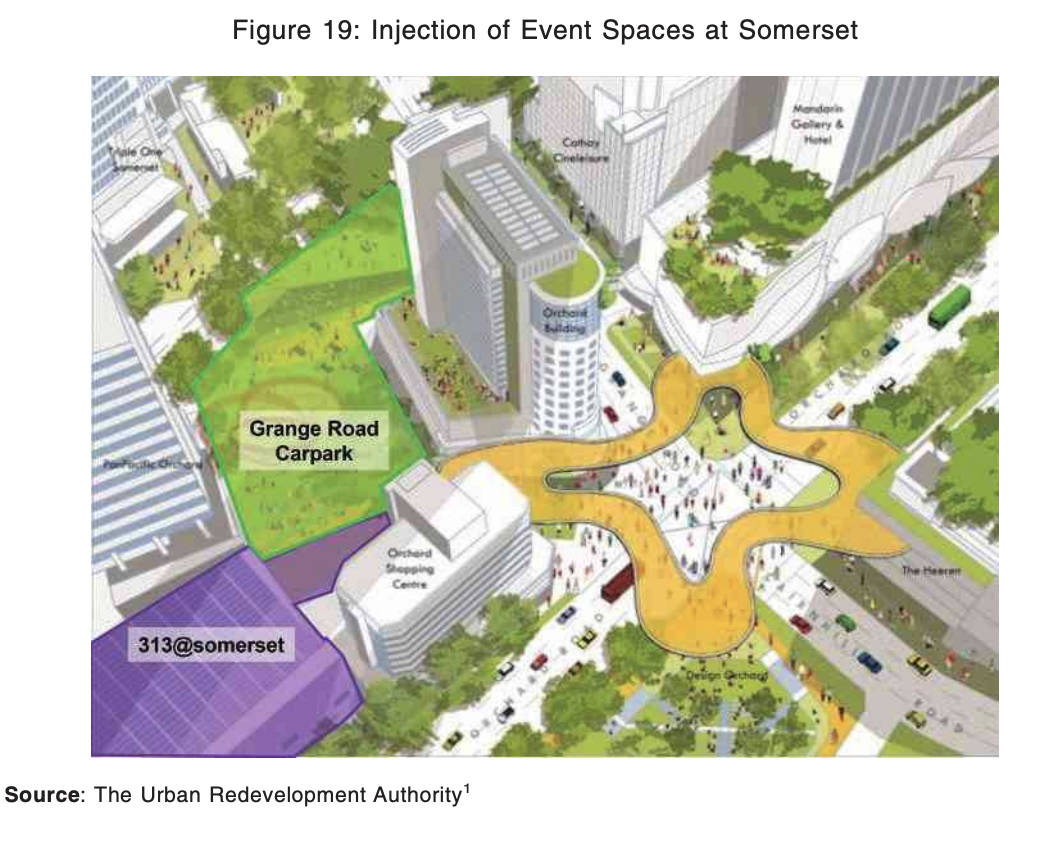

For Somerset 313, the Singapore government and Orchard Road Business Association is working on a revamp in the Orchard Road/Somerset area, so this could bode well for the property in the near future.

For Sky Complex, investors might be interested to know that Milan is the fourth largest economy in Europe, and also one of the top destinations for the office sector. Rents in such Grade-A offices are projected to increase over the next few years, but since Sky Complex is already tenanted to Sky Italia on a long-term master lease of 24 years (till 2032), the main gain to watch here could be in terms of property valuation instead. (Sky Italia is the only tenant there, and is owned by Comcast, which is the second largest broadcasting and cable TV company in the world by revenue.) Note that the annual rent collected is 16 million euros, which provides rental income stability.

Risks

With current economic conditions, the retail scene might be squeezed if we were to go into a recession. This would likely lead to a drop in share price, given Lendlease REIT’s exposure to the retail industry as Somerset 313 comprises 71% of its asset portfolio.

But then again, talks of a recession have been looming since 2016 and it hasn’t yet happened, so there’s little use in freaking out over what’s yet to come.

Conclusion

With the hype over this IPO, it should perform well in its opening week, but how its share price fares later are anyone’s guess.

I reckon that most investors who choose to subscribe at this stage might be holding on, given the opportunities in its Sponsor’s pipeline of assets. I’m looking forward to the Sponsor injecting newer assets in the next few years for the REIT, given their global ambitions outlined in the IPO Prospectus.

The net asset value of this REIT is $0.81 but the IPO listing price is at $0.88. What this means is that retail investors will be paying a slight premium if you were to subscribe at this stage. You will have to decide for yourself if the brand name and Lendlease’s track record warrants such a premium. I certainly think it does.

So, in summary, here are my 3 reasons why I’m subscribing to the Lendlease REIT IPO:

- A decent premium to valuation (8%)

- A strong pipeline of opportunities

- A strong list of cornerstone investors

I’ll be sizing the proportion this takes in my portfolio as I hope to add more units at a lower price if it falls after the hype settles down.

With love,

Budget Babe

2 comments

Just my opinion, it seems like Lendlease is just using the listing as an opportunity to dump 313 Somerset to the REIT would-be investors. 313 constitutes 65% of the portfolio by NPI and has a woefully short WALE of 1.6 years. Considering the current retail environment, the impending economic slowdown, the ongoing trade war, and the fading lustre of Orchard, it seems that Lendlease is simply trying to milk a fast cash cow.

Moreover, if you look at Starhill, it is trading at 15% discount to NAV for, IMO, a superior mall asset. Makes little sense to pay over valuation for a REIT that is in substance (65%) just another orchard-based mall.

If JEM was included, it might have sweetened the deal slightly, but for now, I think I would pass.

What their motivations are is anyone's guess. I'd like to give them the benefit of the doubt though, because if this IPO was simply their exit strategy then they probably would have structured some of the terms quite differently than what they've done here.

Agree that if JEM, or even PLQ, was injected then it would have been more attractive.

I did compare it to Starhill REIT, but it isn't really an apple to apple comparison imo given the asset classes. For one, Starhill's performance hasn't been exactly great, and they haven't demonstrated their prowess enough for lease retention, management and rental escalation. In contrast, Lendlease's master tenancy agreement with Sky Italia gives an assured base for a very long time. Starhill does not have this.

Lendlease also has a good pipeline of assets from its Sponsor which I'm looking forward to, which Starhill doesn't really have.

Instead of choosing between both, why not have both? 😛

Comments are closed.