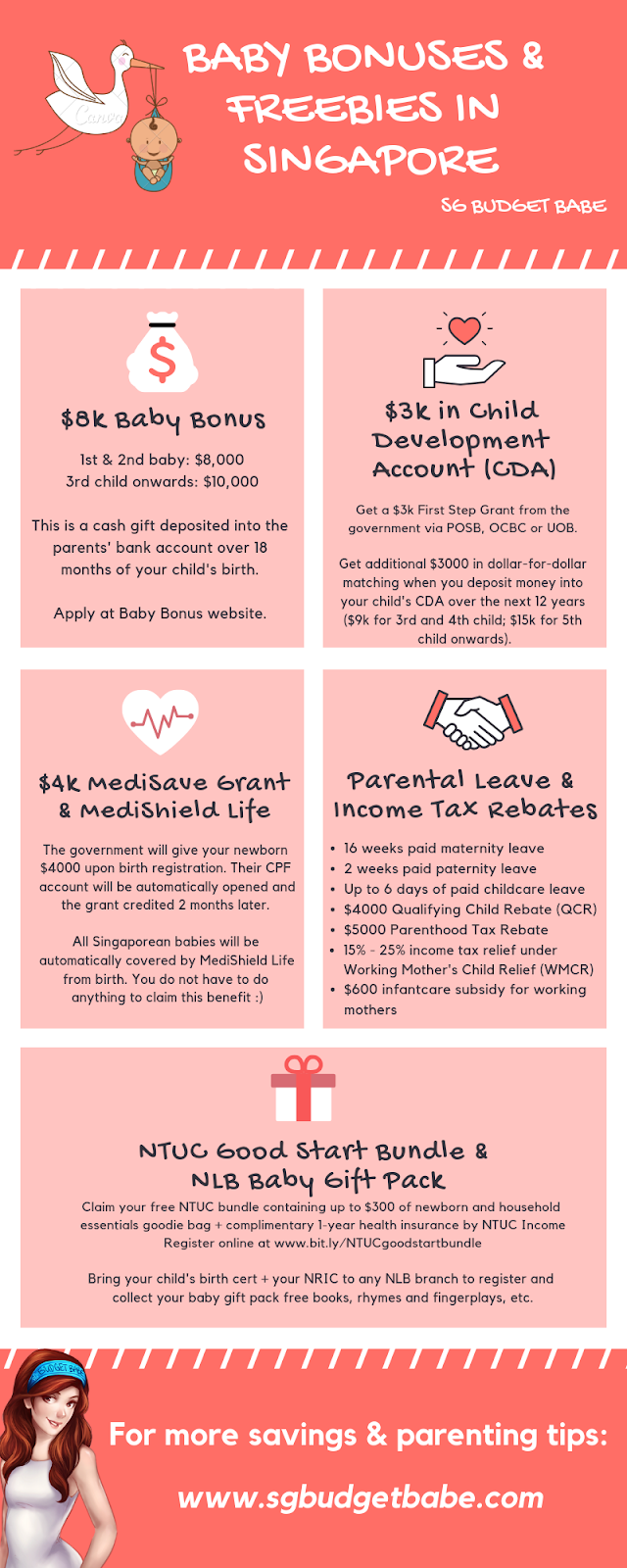

There’s a wide range of benefits available to parents if you’re having your baby in Singapore. I came to learn of all these cash grants and freebies when I was pregnant with my first child, but realised that many of my peers aren’t fully aware of what they’re entitled to, so here’s a full list of what you can get and how:

I detail them below on what they cover, and how you can apply to claim your benefits:

- The Baby Bonus cash gift

- The First-Step CDA grant and dollar-for-dollar matching

- MediSave Maternity Package

- MediSave Grant for Newborns

- MediShield Life Coverage

- Parental Leave Entitlement (paid by the government, too!)

- Income Tax rebates

- NTUC Good Start Bundle (with free hospitalisation insurance)

- NLB Baby Gift Pack

1. Baby Bonus Cash Gift

As part of their efforts to boost the population fertility rate, the Singapore government gives you at least S$8,000 in cash if you’re having a baby and doing your part for “national service” :p

Expect to get:

- $8,000 for your first and second child

- $10,000 for the third child onwards

The cash will be paid out over the first 18 months of your child’s birth. You can expect to receive the first portion of the cash gift within 7 to 10 working days of your child’s birth registration (I got mine the week after applying), and after completing the online form found here. The cash can be used to offset your newborn’s expenses, although they may not necessarily pay for everything you need to spend on.

2. Child Development Account (CDA)

There are two parts to the CDA:

- A first-step cash grant of $3,000

- Dollar-for-dollar matching of $3k – $15k (depending on your child’s birth order)

You can expect your child’s CDA to be opened within 3 – 5 working days of their birth registration among either of the local banks – DBS, OCBC or UOB. Save a trip down to the bank by doing it online here.

For the dollar-to-dollar matching, you have till your child turns 12 years of age to contribute and get the equivalent from the government. The sum will be credited in the subsequent month of your top-up.

In our case, we chose to open the CDA with POSB (for reasons detailed in the above linked blog post). Within a few days, the new account was opened for us, and we received the NETS card by mail shortly after. I then got an SMS saying that the $3000 CDA First-Step Grant would be credited into my account soon. Everything took about 2 weeks so it was pretty efficient!

- Up to $900 for pre-delivery care (bring receipts of your prenatal consultation visits, screening tests, etc and submit to the hospital at time of bill payment after your delivery)

- $750 to $2,150 for delivery procedures

- $450 to offset each day of your stay in the hospital (usually 2 days for vaginal deliveries, and 3 days for Caesarean)

For my baby’s bill, $900 was deducted from my MediSave.

4. MediSave Grant for Newborns

- 16 weeks of paid maternity leave for mothers (as long as you’ve served in your job for at least 3 months), or 12 weeks of paid adoption leave

- If you’re self-employed, your benefits differ and you generally get 8 to 16 weeks of paid income – read here to calculate how much you can get (hint: it depends on how much income you declared, so if you have been under-declaring your income to avoid taxes…good luck on that!)

- 2 weeks of paid paternity leave for fathers

- 4 weeks of shared parental leave (if your wife is willing to transfer hers to you)

- Up to 6 days of paid childcare leave for each spouse, if your child is younger than 2 years of age (the Government-Paid Child Care Leave Scheme) – however, do note that this is subject to agreement with your employer as well, so if your workplace is not entirely pro-family then this could be quite tricky.

- You’ll get 2 days if your child is between the age of 7 – 12 years

- 6 days per year of unpaid childcare leave per spouse (thus combining with the above paid childcare leave, you’re entitled up to 12 days if your child is younger than 2 years old)

6. Income Tax Rebates

Take advantage of the different tax rebates available for Singaporean parents :

- Qualifying Child Relief,

- Claim up to $4,000 per child if your offspring is younger than 16 years of age or studying full-time.

(Tip: the spouse with the higher income should be the one claiming for this, as it could probably reduce his/her taxes by a larger margin!) - Working Mother’s Child Relief,

- For mothers who are working and handling dual roles, you can claim 15% of your earned income in tax reliefs for your first child, 20% for your second, and 25% for each child if you have 3 kids or more!

- Parenthood Tax Rebate,

- On your first child, you can claim $5,000 of Parenthood Tax Rebate. If you have 2 kids, add on another $10,000 for your second child. Or, if you’re like my cousin with 3 children (or more), you can add on $20,000 more for each subsequent child. This works out to a significant total of $35,000 of tax rebates if you have 3 children and make the maximum claims for them!

- Foreign Maid Levy Relief,

- If you’re hiring a domestic helper to assist you

- Grandparent Caregiver Relief

- If your parents are unemployed and helping to look after your child

For full details on claiming these income tax rebates and other methods to reduce your income tax, see this post I had previously written here, which was also shared by Ho Ching herself!

7. Subsidized Infant Care Scheme

You might need to place your newborn in an infant care centre once you go back to work, especially if you don’t have a domestic helper or a parent to help you look after your child. Fees aren’t cheap; on average, expect to pay at least $1,300 every month (for each baby). PCF Sparkletots and My First Skool have the most number of branches island-wide, and are generally affordable options for you to look into for a start.

If you enrol your child in a centre licensed by the Early Childhood Development Agency (ECDA), then you’re automatically eligible for a subsidy. Working mothers can get a basic subsidy of up to $600 to offset your monthly infant care expenses, or up to $300 at childcare centres. Families with non-working mothers get up to $150 per month.

The last 2 I’ll be sharing below aren’t exactly given by the government, but I’m including them in this article as they’re from a national co-operative and a government statutory board.

8. The NTUC Good Start Bundle

An initiative put together by NTUC and its 8 social enterprises, parents of newborns can claim up this bundle containing up to $300 worth of newborn / household essentials and benefits.

|

| My NTUC Good Start Bundle, which I received for my firstborn |

It also comes with a free one-year health insurance coverage, courtesy of NTUC Income. Don’t forget to register for your free bundle here once your baby is born!

- 3 board books

- Reading is Fun! Publication

- Rhymes and Fingerplays for Little Ones

- Baby Height Chart

- A Guide for Reading with Little Ones DVD

Parenthood isn’t easy, especially for first-time parents, so don’t forget to register and claim all your benefits and entitlements as listed above to help make your journey a little easier!

With love,

Budget Babe

4 comments

good stuff… i came across heartland boy blog, which his newborn was not covered by medisave for the first 14 days. his new born had fever and medisave nor any pte insurance dont seem to cover.

is this something that is lacking for newborn coverage?

hmm based on what I know,

MediShield Life = available in first 14 days, but only in lower class wards for infants. if one opts for a higher class ward or private hospital, then the bill won't be subsidized (or as much)

MediSave = should be available leh to withdraw for hospitalisation! not 100% sure on this though but it should be right? happy to stand corrected.

private insurance = no. I've written about this before in a previous post recently, also extracted here: "Do note that the earliest you can buy insurance plans for your child is after 14 days (but not if they have jaundice, in which case you've to wait until the jaundice has been completely cleared), so if you want any hospitalisation coverage for your newborn during the first 0 – 14 days of birth, only a maternity insurance plan will offer you that (but there are apparently no insurers who cover for jaundice"

https://www.sgbudgetbabe.com/2018/07/what-are-top-5-insurance-plans-that-you.html

which is why it is CRUCIAL to get hospitalisation insurance i.e. an integrated shield plan on Day 15 if parents can, otherwise, do it the moment the jaundice is cleared!

https://heartlandboy.com/integrated-shield-plan-for-your-child/

i think you are right, i could have misread.

"However, MediShield Life did not come in particularly useful in this situation as well. According to the Paediatrician, an infant as young as 9 days old should be staying in an isolated ward as far as possible (in other words, as long as parents could afford it). As her immune system was still very low, there was every chance that Baby Olympia could contract other infectious diseases from her co-patients in the ward. That would add to further complications and Heartland Boy is certain that no parent would want that on their child. Therefore, on the advice of the Paediatrician, Heartland Dad opted for a class A ward in a restructured hospital. As a result, Baby Olympia’s hospitalization stay was not entirely subsidized under MediShield Life."

nonetheless , there is This 14-day private health insurance gap is indeed very annoying and something that is beyond the control of parents.

there's a solution to bridge the 14-day gap : global health insurance, which requires you to buy usually at least 12 months BEFORE pregnancy and premiums cost $6k+ annually when I got quoted for it this year. which means…if someone suay suay buy liao but takes longer than 12 months to conceive successfully, they could end up paying a lot more.

that's the solution to bridge the pregnancy delivery costs insurance gap that I've mentioned in my articles too. cos private insurance won't cover cost of delivery for pregnancy here, unless due to one of the listed pregnancy complications >.<

Comments are closed.