Wow, I wasn’t expecting so many of you to appreciate my previous post on reducing your income tax – thanks for the support! Remember to maximise your tax reliefs and deductions every year, so you’ll end up saving up to thousands of dollars with just a few minutes of work!

To all the new readers who just visited this space because you got directed here from Ho Ching or IRAS, hello!

Anyway, as a continuation to the earlier post, now that we’ve explored the various ways to reduce our income taxes, the next step to look at would be the mode of payment. Should you opt for monthly repayments or a one-time yearly bill? Should you use GIRO or your credit card?

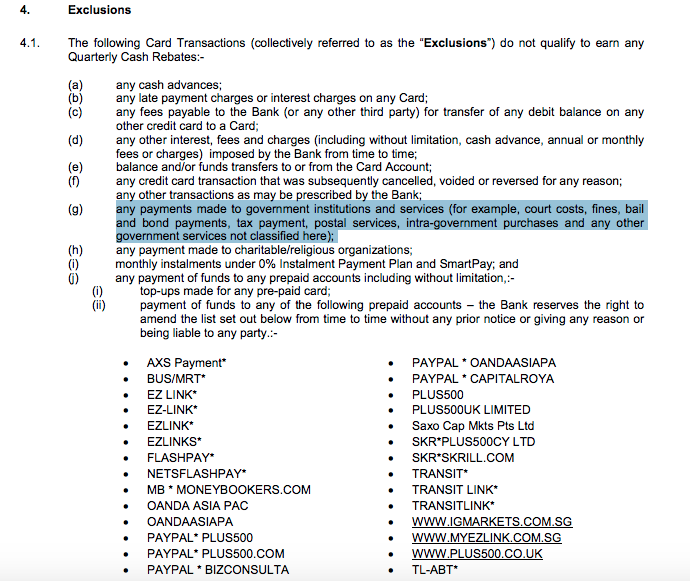

Unfortunately, if you’ve ever tried paying for your cashback with your credit card in a bid to earn cashback or miles, you would have probably realised by now that tax payments (as well as that to government organisations) are usually excluded from these rewards.

Even the SCB Unlimited Cashback card, which I’ve previously reviewed and raved about here (seriously, go get one now if you haven’t already! What’s more, get $270 in cold hard cash if you apply for one before 30 April 2018 here), excludes tax payments from cashback as seen in their exclusion clause 3j.

You see, most of the banks and credit cards reward based on discretionary spending i.e. products or services that you want to buy instead of the stuff that you need. That’s why categories like dining and shopping get such generous cashback / miles rewards, because you could technically live without eating out and buying new stuff.

As such, one glaring gap in my credit card strategy was in how I could never get any rewards back on my mandatory spending, such as when paying for income taxes, insurance and clearing off my loans. It was frustrating to see how I wasn’t able to get anything back on the expenses I couldn’t avoid every month!

Until recently, that is.

Those of you who have read my Guidebook to the Best Cashback Tools in Singapore should be familiar with how much I’ve raved about CardUp since discovering them months ago.

With CardUp, you can now pay for insurance premiums, rent, school fees, condominium charges, income taxes and get cashback / miles doing so!

How CardUp works

If you study the T&Cs of most credit cards, you’ll realise that no miles or cashback are given for payments made to government agencies, insurance premiums, ez-link top-ups, donations to charitable organisations, etc. CardUp basically enables you to make single or recurring payments online via your credit cards on these spending categories where you couldn’t previously use your card.

Now, this is a big game-changer because prior to CardUp, there was no other service or tool that allowed you to do this! Previously, you could only pay for your rent, mortgage and other mandatory expenses through bank transfer, cash or cheque options. This eliminated a huge chunk of big-ticket spending that can actually help you rack up significant credit card rewards.

There is a 2.6% processing fee imposed (due to the banks and credit card fees), so it is vital that you choose a card that netts you positive rewards even after paying this.

What if the recipient doesn’t accept credit cards?

CardUp does a bank transfer to your recipient, so it doesn’t matter whether or not they accept credit card, and neither do they need to be registered with CardUp. This is what makes CardUp such a fantastic solution, and I only wish I discovered it sooner.

CardUp already has many recipients on its platform, but if you still can’t find yours, all you need to do is to set up a new recipient so that the transfer can go through. In addition, you can even set up recurring payments so you don’t have to log in every month just to transfer.

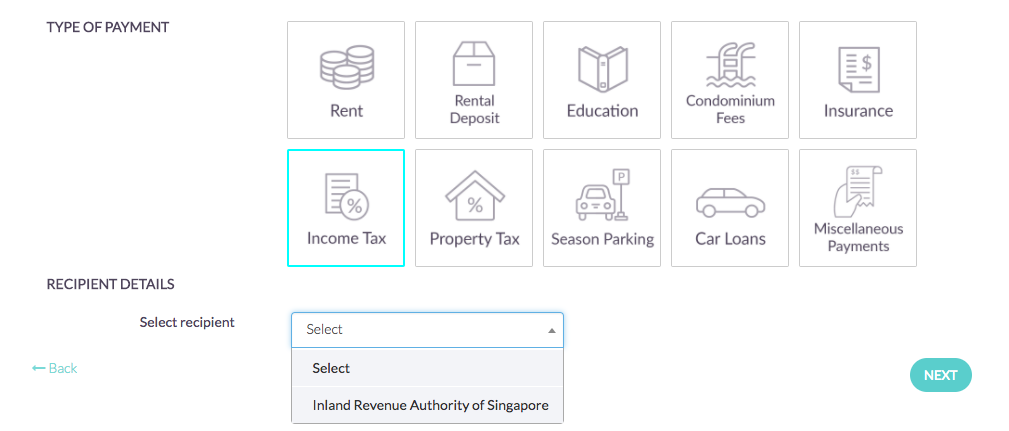

What you can use it for

- Paying your income tax, property tax or utility bills

- Insurance premiums

- School fees (childcare, secondary schools, universities and private institutions)

- Condominium fees

- Charity donations

- Car loans

- Rental

- and more!

Sounds good! Which cashback card should I use on Cardup then?

The best strategy would be to use a cashback credit card that gives you a higher rate than CardUp’s service fee in order to net positive cashback.

The best strategy would be to use a cashback credit card that gives you a higher rate than CardUp’s service fee in order to net positive cashback.

Here are the cards I would recommend to use with CardUp:

UOB OneStandard Chartered Manhattan(SCB is no longer accepting new signups for this card, which is a huge pity, but if you were lucky enough to get your hands on it previously please maximise it!)- BOC Family

- Maybank Platinum Visa

July 2022 Update: UOB One has also recently announced CardUp transactions will now be excluded from earning cashback

You can also check out their cashback calculator here first to calculate the amount of cashback you’ll get when you pay via the recommended cards!

Before CardUp broke into the scene, I was paying for my tax bills either through online or at the AXS machine, but now I’m opting for repayments via CardUp in order to get my credit card rewards.

Before CardUp broke into the scene, I was paying for my tax bills either through online or at the AXS machine, but now I’m opting for repayments via CardUp in order to get my credit card rewards.

I don’t want cashback! Which miles card should I use on Cardup?If you’re collecting miles for your next *free* flight(s), here are the miles cards which I favour and would recommend to use with CardUp:

- AMEX Krisflyer

- Citi PremierMiles Visa

- DBS Altitude Visa Signature

- UOB PRVI Miles

You can also check out their miles calculator here first to calculate the amount of cashback you’ll get when you pay via the recommended cards!

So when you pay for your income tax bills from next month onwards, don’t forget to route them through CardUp so you can chalk up more cashback / miles while doing so!

For readers looking for a further discount, I’ve reached out to CardUp and they’ve offered $20 off your first payment fees when you enter the promo code “SGBUDGETBABE“.

Always remember, credit cards can be your best friend if you know how to use them well! You can read more about maximising cashback tools in Singapore here on my previous post too ; have fun!

Note: This post was written in collaboration with CardUp.

Note: This post was written in collaboration with CardUp.

With love,

Budget Babe

20 comments

using BOC family, which category does it fall under for insurance premiums and taxes?

reason i am asking is coz, if it falls under "others", then you get 0.5% CB only

sorry, i was playing ard the Cardup website and notice it says that it falls under the "online" category.. hence there is a $30 cap

I couldn't reply you while at work! but haha in my research previously I noted it as being under the "Online" category, so unless BOC has changed their classification since, then it should be 5%!

no worries BB.

btw, the $20 promo is only for 1 payment right?

so you will need a min payment of 769, in order to utilise the entire 20 rebate?

correct me if i am wrong.

yup only to offset the fees for your first payment via CardUp!

Hi, if I pay the IRAS tax with CardUp, do I need to cancel my existing GIRO?

wow, but 800 for one payment seems quite a lot. haha…

may i know what you use it for?

Hi there, I read this post with great interest as I thought I could pay my insurance premiums (one of my bigger expenses at the moment which gets me no cashback) with CardUp. As such I looked around on forums as well and it looks like good cashback cards such as DBS LiveFresh and OCBC 365 do not count Cardup as an eligible transaction. Have not dug deeper but that mainly leaves the 3-4 cards mentioned in your post, out of which the BOC one offers any significant gain after the CardUp fees. But then BOC card has a cap which only allows me to spend up to $600 to make the best of it. This leads me to the next issue I have. I choose to pay my premiums annually as it is cheaper, however such lump sum payments tend to far exceed the cashback caps of most cards. Can CardUp pay my premium in annual form but deduct from my card in monthly form? If i had to start paying my premiums monthly to keep within the caps, I doubt the cashback (after CU fees) would offset the more expensive monthly premiums. Just my 2 cents. At this stage I do not have anything else on CardUp's list to pay for except income tax, therefore CardUp at this point is not useful to me.

income taxes and insurance premiums currently, exploring season parking for my husband now that I'm the one helping to make his payments (cos he always forgets!) next time when i have kids, I'll use for their education as well!

yes lol otherwise you pay twice !

Hi! I've actually already specified in this post that the only cards I recommend people to use with CardUp are UOB One, Standard Chartered Manhattan, BOC Family and Maybank Platinum Visa. You're right that DBS LiveFresh and OCBC365 aren't included because they wouldn't fit into this hack for that very reason!

"This leads me to the next issue I have. I choose to pay my premiums annually as it is cheaper, however such lump sum payments tend to far exceed the cashback caps of most cards."

At the moment you're getting absolutely zero cashback for your insurance premiums, as you mentioned yourself. I guess it depends on your insurance premium, because my annual premiums on all of my insurance policies don't exceed the cap, except for one. Everyone's insurance policy (and thus premiums) differ so you definitely have to see whether this is a good hack for you. However, I wouldn't explore monthly payments unless the fees and cashback earned actually justify it. In addition, like you said, you're currently paying annually and getting zero cashback, but if you go through CardUp you can at least get SOME cashback even after fees, even if it doesn't mean your entire premium amount entitles you to the full cashback since you exceed the cap. Comparing the before scenario (zero cashback) vs the current option (some cashback, although not on the full premium amount), I don't see why not since there's a tangible benefit there.

I paid my income tax annually last year as a one-time payment and obviously didn't get the full cashback on it due to my card's cashback limit, but comparing to before where I get absolutely NOTHING, I still think this is a way better option.

" Can CardUp pay my premium in annual form but deduct from my card in monthly form?"

I'm not sure, you might want to direct your question to CardUp themselves to get a B&W in writing, but my simple guess is no, this wouldn't work.

Hope that helps! At the end of the day, we need to be savvy and assess the tools for our own financial circumstances to see whether it works. It certainly does for me, and for many of my friends whom I've already recommended it to, so whether or not you can make it work for yourself will depend on your mindset and approach! 🙂

Thank you for taking the time to reply! Your recommendation came across exactly as it is – a recommendation. I had the impression that I could use other cards as well, so of course this revelation puts a little dent in my plans.

I did pose my question to CardUp themselves, and they said they do not do such things. However, from forums, apparently it is possible to pay partial payments of your annual premium in advance of the actual due date.

I am still quite interested in this hack, but at the same time I'm a bit wary about having to sign up for one more card just for this (I already have 6 trying to maximise my cashback).

On a side note, do you have a past post about your insurance portfolio? Otherwise, care to share? I'm curious to know how your annual premiums don't exceed the cashback cap yet can keep you adequately protected.

Thanks for your time again!

I apologise for adding on further. Regarding this point "but if you go through CardUp you can at least get SOME cashback even after fees, even if it doesn't mean your entire premium amount entitles you to the full cashback since you exceed the cap. Comparing the before scenario (zero cashback) vs the current option (some cashback, although not on the full premium amount), I don't see why not since there's a tangible benefit there" It's only useful if the full premium amount does not exceed $1153.85 – using BOC Family which is capped at $30 cashback, the CardUp fees for this premium amount is also $30.

Hi BH!

Definitely, I would also be wary about signing up for one more credit card especially if you're only going to use it for just CardUp alone! Sounds a little like too much hassle if there's no other use for it, haha.

Interesting to know that they mentioned they don't do such things! Do you mean people on forums have said they tested it out and it works with CardUp?

Nope, I've not done a post about my insurance portfolio yet…although I probably should soon, good recommendation! 🙂 The reason why my annual premiums don't exceed is because I'm using CardUp to pay for both my term + CI and term policy at the moment (at different times), and each of them costs less than $1000! (the second one being much cheaper since it is a pure term and low coverage which I bought years ago, whereas the one with CI was bought after I got married!)

so that's how I still get a net positive 🙂

Oh and on your point regarding the fees, please feel free to offset $20 from your CardUp fees by using my promo code SGBUDGETBABE if you'll like! 🙂

BH, I have another recommendation! If cashback doesn't work for you, are you concurrently also collecting miles? because there are quite a few good miles card that you can use with CardUp as well (and less limited than the cashback options!) TheMileLion has written about this before, although from a quick glance it seems like many of the banks have also revised their terms to exclude CardUp since -.-

http://milelion.com/category/ipaymycardup/

if you wanna read and explore the miles rewards instead!

Thanks BB for your replies!

Regarding splitting of payments, you can schedule as many payments as you like on CardUp. On the insurer's side, usually they need to be informed that you are paying your premium in advance. So for example, if I have a 2k premium due in Sep, I could supposedly pay 500 per month for the next 4 months. Have not tried this myself before but it's what I read on the forums.

That promo code can be helpful! But what about subsequent premiums that I will be paying many years down the road? I guess one CardUp payment is better than none at all 🙂

Oh no I just did the math again. My premium cannot exceed $1923.08 otherwise the 2.6% fee will negate the $30 cashback + $20 offset. Looks like I have to call up my advisor and find out more about partial advance payments :/

Sadly I don't have enough moolah nor expenditure to do "concurrently" (which is why I read this blog right 😉 ). Personally I'm not much of a wanderluster, not to mention miles only gets you the air ticket but then there's still more expenses to fork out once you decide to go on a trip. Therefore I'm purely a cashback guy 🙂

Hi! I'm currently trying to set up monthly payment through cardup to pay for my income tax but only one-off frequency payment type can be chosen.

In this article you have written "I'm opting for monthly repayments via CardUp in order to get my credit card rewards". Do you mean that you set up multiple 'one-off' payment for different months according to the IRAS giro installment plan for income tax?

Hi Jace!

I only started using CardUp for the first time last year, and since my tax bill arrived in November, I used CardUp for a one-time payment for the entire tax bill in one setting. For this year, I've not gotten my income tax bill yet (just filed it last month anyway) so I'll have to wait until that arrives to try it out.

I've always only seen one-off frequency for the type of payments I've made through CardUp so far, so I cannot be too sure, it might be better to ask the CardUp team directly?

Thanks for pointing that out though, let me amend to reflect better clarity of the sentence!

Comments are closed.