How should I read the numbers on my Investment-Linked Policy (ILP)?

I lost more than 2 months worth of salary to learn this important lesson: when insurance and investments are bundled together into a single product, the consumer is often left worse off.

A few years ago, when I was a naive fresh graduate in my first job, I met a friend of mine to understand more about financial planning and insurance. My knowledge then was limited – I knew I needed to invest and buy insurance, but I didn’t know what was essential to get. Furthermore, at that time all I wanted to focus on was to put in my best effort at work so that I could get promoted and climb the corporate ladder.

Insurance was the last thing on my mind. So I went with my friend’s advice, thinking that as a financial advisor, they’ll probably know better than I. He recommended me an ILP, I briefly read through the policy and asked some questions, and then I stupidly thought I knew everything. I didn’t quite know how to read the benefits and premiums table, so I simply took him at his word.

A few years passed and my career reached a more stable stage. I then decided to take a second look at my policy, and was shocked when I learnt how to read the numbers and realized the hard truth of what I had signed up for.

I signed on the above, but did not truly understand what I was committing myself to. The terms and conditions were NOT clearly explained to me in the way I’ve dissected it below, and if I had known these earlier, there was no way I would have signed up for such a plan.

Regular readers will know that I announced on my blog sometime back that I had cancelled my ILP policy, but I’ve never gone into details to explain why I did so. Part of the reason was also fear – I was worried that if I reveal this, I’ll get screwed over by insurance agents on my blog or even sued by insurance companies for ruining their rice-bowls. Back then, there weren’t as much people writing about ILPs as there are today. But despite more information, there still isn’t a resource from a consumer point of view on what these ILPs really mean to an individual, so I’ve decided to finally share my story about why I cancelled an ILP plan that didn’t work for me.

For confidentiality, I will not be sharing the name of the plan I bought.

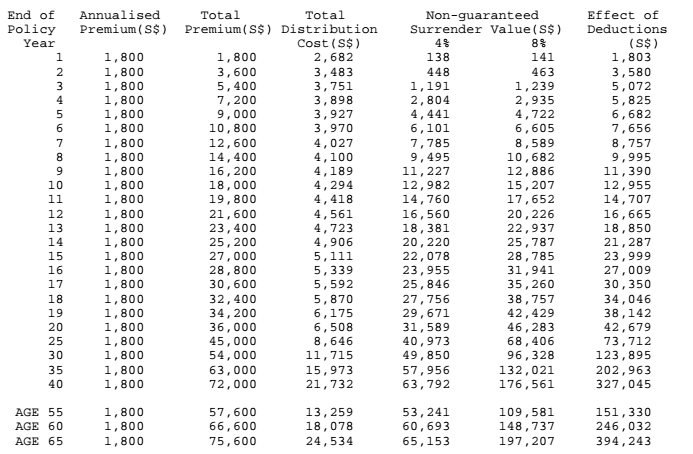

This table above is the benefits illustration table. If you compare columns 2 and 6 (where my agent pointed me to), the policy looks good, doesn’t it?

Put in $72,000 over 40 years and get $176,561 back! That’s $100,000 FREE!

What I didn’t know then was that if I put my money elsewhere, at 8% I’ll be getting $500,000 instead – FIVE TIMES MORE! (Remember this figure, I’ll come back to this later.) But of course, my agent didn’t tell me this. To give him the benefit of doubt, I’m not sure if he even knows such an alternative (easily) exists?

Add up both figures and you’ll get $500k. Now do you know why I said earlier that I should be getting $500k back instead for the same amount of money invested?

In fact, here’s something even better. Instead of giving away that $10k+ to get insurance coverage on this plan, I can easily get a $300k protection plan for even cheaper ($8550).

So that’s my full story of why I cancelled my ILP and decided to buy term, invest the rest.

I don’t know how many people will see this, but at least now the Internet has gotten one more resource from a consumer point of view why I personally think ILPs are the worst financial instruments ever created. The consumer, like what I’ve experienced myself, only stands to lose in almost every circumstance.

If you’re thinking of buying an ILP or know of someone who does, I hope this resource has helped you understand a little more. Unfortunately for me, I had to forgo 2+ years of premiums to learn this lesson because this didn’t exist before.

With love,

(a poorer)

Budget Babe

31 comments

hi

i want to ask term policy is only upto 65 yrs old whereas life policy is till death do us apart

is the 65yrs old age limit an issue for term ?

No longer an issue. I've written about this myth in a previous post, you can find the link below! Hope that helps 🙂

http://sgbudgetbabe.blogspot.sg/2016/08/should-i-buy-term-or-whole-life.html

Hi, I wrote something related to this to spread the knowledge as well: https://www.scribd.com/document/270574745/Of-Investing-in-Unit-Trusts-and-Investment-Linked-Polices-ILPs

This a great resource for everyone looking to increase their financially literacy. There is a strong conflict of interest between financial institutions and the clients.

It's well known that banks and insurance companies make their money through fees. While a 1% annual fee doesn't look much, over time, they tend to accumulate. The fees will significantly cut into your returns.

I've written an article on why you should care about your own money.

http://www.livingafreelifetoday.com/blog/nobody-cares-about-your-money-more-than-you/

My wife and I bought a few policies from prudential and they are heavily taxing us monthly.

Can I request that you help look through and advice as a third neutral party to save us? Appreciate.

My wife and I bought a few policies from prudential and they are heavily taxing us monthly.

Can I request that you help look through and advice as a third neutral party to save us? Appreciate.

Hi Dienth, thanks but I dont think I'm in a position to advise as I am not a licensed agent. Perhaps you would like to reach out to a licensed practitioner instead? Or I could recommend you my agent if you like, he's quite trustworthy and tells me everything about fees incurred.

Who have not been "fooled" at least once by some form of purchased insurance is indeed very fortunate!

While it is true that we should not mixed insurance with investment yet for me i always very interested in the column of "Guranteed Surrender Value"

Though again we should not mixed investment with insurance, as an investor we can't help comparing.

We know then indeed insurance is insurance, investment is investment.

But under special circumstances some forms of insurance is needed for mentally impaired, born blind,…..one word-Special Need Children.

Their parents won't be around for ever.

i think insurance companies have not served (aka capitalised) fully on the needs of this special needs children.

I was thinking of surrendering my ILP as well. Was 90% sure i am going to do it. After reading your entry, i am 110% sure. Sadly this is after 4 years plus. Argh. But better late than never i guess!

being an ex insurance agent myself, i believe i would be in a better position to point things in a different light.

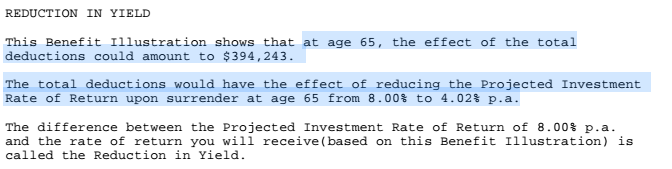

firstly, i guess u dont really understand what is "effect of deduction". if you think just abit more, how are you able to lose 300k when your total outlay for 40years is just 72k? effect of deductions takes into consideration of the total amount of money you paid in terms of commission and fees adjusted with an interest rate. that is why u see between year 35 and year 40, "effect of deduction" increase by over a 100k.

and if you are talking about taking up term plans for the same coverage, just do take note 1st before u start to regret a few years from now, term plan doesnt have any surrender values in it, nor does it gives u the flexibility of what an ilp does.

cheers!

I'm glad this helped you! I only regret not knowing this sooner – maybe then I wouldn't have bought my ILP.

Maybe…could it be that it isn't as profitable? *shrugs*

Thanks for weighing in! Always good to get a counter-opinion.

I've already explained the numbers in detail above so I won't repeat that on "how are you able to lose 300k when your total outlay for 40 years is just 72k"? You can scroll up for the answer and calculation breakdown.

I don't think I'll regret that my term plan doesn't have any surrender value on it 🙂 there's no surrender value on my healthcare insurance either, so why should there be one for my life? Folks who want surrender values on their life insurance are welcome to purchase ILPs but that's just not for me.

If I want flexibility, I won't look at ILPs, I'll look at bonds, ETFS, and other direct investment vehicles myself 🙂 cheers!

Insurance agents…housing agents…I wont detail how much I dislike dealing with them. Suffice to say I'm glad that the age of the internet is here. We don't need "agents" pushing high cost (and even higher conditions on claims so that payouts are "not covered") policies/services when we can do a better job doing it ourselves.

Great article Budget Babe! I'll be seriously relooking my ILPs in 2017… Hmmm….

Great article! I also share the same view as you after I start to learn investing and money management. After reviewing my ILP with GE this year, although the underlying funds I am in are growing, I realised the hefty fees and commissions are eating in the returns in the long run, and that's a great opportunity cost. This year is my third year, and I am going to cancel it. I will also forfeit around $5k premium, and I will take this as a lesson learnt that one has to be in charge of his own investment and financial planning.

Glad to hear that you found this useful!

I lost a 4-digit figure too. Heart pain, but well worth a good lesson.

Definitely this article provide good knowledge of ILP, and I strongly support buy term and invest the rest also. But it always hard to convince people to believe in that and ILP is a good product for people who are busy and no much investment knowledge. So I just point out a few mistakes or misleading information for those who still prefer ILP.

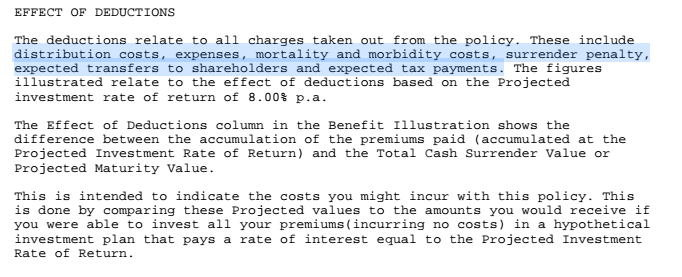

1. “ I'll be getting $500,000 instead. The answer lies in the high costs charged to the consumer for the ILP. ”

The main costs that affect the return of the policy is distribution costs and mortality and morbidity costs. Distribution costs are the costs to make the plan available to the public, like commission, costs of benefits and services paid to the distribution channel. Mortality and morbidity costs is the insurance charge. Means to protect you or your family financially when Death, TPD, Critical Illness occurs. So the old your age, the higher sum assured you get, the more insurance charges you need to pay. While smoking status and gender also affects. Usually the insurance charges has a much bigger impact on the return of the policy than distribution cost. But definitely not for the case here. Don’t know why the distribution cost is unreasonably high. I do a similar quotation of AIA product, the distribution cost is much lower. On the end of policy year 40, the total premium is 72,000, distribution cost only 5557, return based on 8% will be 252,700, effect of deduction is 250,915 based on 8% return.

If you ever study any economics subjects, this “Effect of Deductions” is similar to opportunity cost. Let’s say if there are two options: marry A or B. If marry A, you get 10k; If marry B, you get 20k. The opportunity cost for marrying A will be 10k, but maybe you love A more. ILP provide protection, while purely investment give more returns. Definitely buy term and invest the rest is a better strategy in terms of returns. But that requires a lot of time, effort and knowledge or an excellent agent.

Actually most of people marry C, save to the bank with interest rate about 0.05%. Means they don’t have any opportunity cost. For typical working Singaporean, who is very busy, ILP is still a good solution. No insurance product is a bad one, just get the one suitable for you.

Hope that my explanation make it clearer about what ILP is. ILP is protection plus investment, it is not fair to simply conclude that you are not getting $500k due to the high costs charged to the consumer. The $327,045 is not charged by insurance company. Due to the effect of deduction (mainly distribution cost and insurance charges), the return is not as much as if you fully invest all the premium without any protection

2. “WRONG. This gets even more shocking: I get back LESS of my total capital even if my money grows at 4% p.a. To be exact, I'll stand to lose $10,447. ”

ILP is a long term plan, if surrender in first few years, the cost will be very high due to the initial cost for the insurance company. It is actually clearly shown in the benefit illustration.

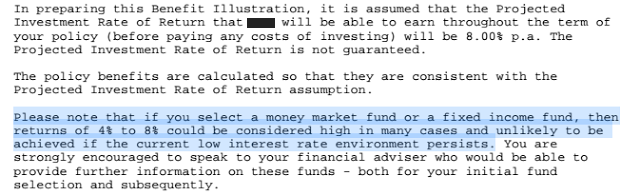

3. In reality, what are the REAL investment returns by these experts? Less than 8%. Check out the data reported by the Straits Times here.

The linked article is actually not relevant to ILP. The fund showed in the article is actually so called par fund, which is linked to saving plans. While for ILP, you need to see the performance of the investment linked funds. Usually you can find the information on the insurance company website. For AIA, you can find it here: http://www.aia.com.sg/en/help-support/funds-information/aia-ilp-fund-prices.html. It you go through all the 30 funds, 8% is definitely quite achievable in the long run.

I am an AIA agent, but the information I shared might be wrong also. Correct me if I am wrong, I am always willing to know more of the products.

Stumbled upon your blog and I agree that there is really very little info on ILP. I analysed the benefit and policy document and I didn't cancel my ILP because I thought I had a chance to save it by reducing the insurance portion to the minimum. I don't know whether I did the right thing because I will only know the outcome in probably 10 years' time, but it looks workable.

Thank you for sharing such great information.It is informative,can you help me in finding out more detail onInvestment In India,i am interested and would like to know more about this field and wanted to understand the basics of Term Insurance Policy

This comment has been removed by the author.

Term policy is quite staight forward, it cover for certain years(for example 10 years)and get lum sum pay out if death, total permanent disability or Critical illness occurs. If nothing happen, no pay out. The advantage is cheap and flexible.

http://www.aia.com.sg/content/dam/sg/en/docs/aia-ilp-funds-overview/latest/AIA-India-Equity-Fund-Factsheet.pdf

Above link is the AIA India equity fund, if you are interested, contact me @ 97906872 and I will share with you more details.

So many people interested in ILP.

How abt i hold a talk on this topic so that all of you can ask questions straight in the face.

To the blogger, there are some misinformation but generally, ILP has high upfront cost.

That again is very general. There are a few variants of ILP and it is a bit complicated to understand it just thru such one dimensional sharing. The good thing abt ILP is customizable, but many agents or practitioners themselves don't even know how to make use of the feature to customize.

I'm a licensed financial practitioner and I don't usually sell ILP. But to said that it is very bad is just plain bias and one dimensional. Have a balanced and well informed session, then conclude whether such product suit you. I don't mind talking about the pro and cons of ILP.

Hi, I would respectfully disagree. I personally am aware of the pros and cons of ILP and have double checked my understanding with various insurance agents, and I believe most of my financial blogger friends do as well. But our stand on it remains unchanged. Do note that we've never said it is a poor product on its own. Our stance has always been that it is unsuitable for us, and for the majority of people who are not comfortable with the high fees charged, and also those who are capable of doing their own investments. Insurance is a product that needs to be customized to each individual, and we've simply highlighted three groups who may not benefit as much from it when there's a better alternative. You could always write your own perspective on it if you think we are being "plain biased" and "one-dimensional", and let readers weigh both views to decide for themselves.

Any insurance agent/financial advisor/other generic "classy" names given to such people who actually believe that an ILP can be better than separating insurance and investment is clearly i) doesn't understand the product well enough or ii) doesn't understand the difference in intent between investments and insurance.

Delric, do share your views here too on why you think ILPs are a good product so future readers can then see both from my perspective and yours when they read the comments 🙂 it'll be good learning for everyone. Thank you!

Hi there, may i clarify that if i were to terminate my 30-year ILP (i'm currently on my first year), would i have to fork out cash to pay the levy or they will deduct directly from the premiums you have paid over the course?

best to ask your advisor on that! and get it in writing

My agent proposed me an ILP last week and she told me that the ILP nowadays is very "competitive" but the figure just doesn't seemed right for me, in fact, it's very similar compares to the figure few years back.

And here i'm again reading ILP related post over internet..

And.. from now on..

Whenever an agent proposed me a ILP, i will always come back here and wake my mind up again!

Thanks Budget Babe!

My agent proposed me an ILP last week and she told me that the ILP nowadays is very "competitive" but the figure just doesn't seemed right for me, in fact, it still very similar compares to the figure few years back. Worth to mentioned that she showed me and insurance cost/1000 sum assured for death and CI which somehow influenced me (i will not say mislead here) to think to consider buying ILP.

And here i'm again reading ILP post over internet..

And.. from now on..

Whenever an agent proposed me a ILP, i will always come back here and wake my mind up again!

Thanks Budget Babe!

Comments are closed.