Insurance

Investing

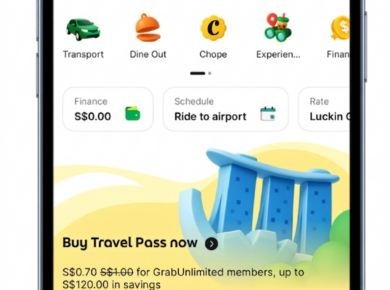

What to do with your expiring GrabCoins

Your GrabCoins may look like small change, but letting them expire is essentially leaving rewards you have already earned unused. Whether your balance is big or small, it is worth checking the GrabCoins catalogue because there may already be something you can redeem.

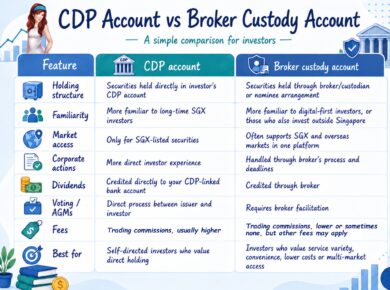

What Is a CDP Account—and Do Singapore Investors Still Need One in 2026?

For decades, Singapore investors have used CDP accounts to hold local shares directly in their names. But with cheaper online brokers and custodian accounts becoming the norm, is CDP still necessary— or is it becoming a relic of the past?

Are Custody Accounts Safe? A Singapore Investor’s Guide to CDP vs Broker Custody

If you buy SGX-listed securities through a broker and they do not show up in your CDP account, does that mean you do not really own them? Here’s what Singapore investors need to know about CDP vs broker custody accounts — and how to decide which setup works better for you.

It will now cost less to buy SGX-listed stocks

Investors who were previously priced out of certain stocks on SGX can now rejoice! The minimum board lot size will be reduced from 100 to 10. Here’s what that means for you.

Short games vs long games

The investor says they’re playing the long game, but then looks at the short-term trader and lusts after their rewards instead. No wonder there’s an emotional disconnect.

Is the monthly GrabCoins Flash Sale worth your coins?

Your GrabRewards are now GrabCoins, and the best time to redeem them might just be during the 15th of every month. During this limited window, your GrabCoins can be redeemed for up to 60% off on food, rides, and other vouchers!

Could the tides be changing?

Last year was the first time since 2017 that international stocks outpaced the US. For the last 5 years, the predominant narrative on social media was to “just dollar-cost average…

Chocolate Finance in 2026: Is it still worth putting money in?

I stayed in Chocolate Finance through the March 2025 chaos. Here’s why I have no regrets and topped up even more money this year.

-1-390x290.png)

A better way for Singapore investors to trade options

We no longer have to stay up past midnight anymore to trade options. Introducing the world’s first pre-market US options trading platform, which is also the only brokerage in Singapore right now that allows you to trade during your after-office hours of 5pm – 10.30pm.

Is it too late to invest in the Straits Times Index today?

The Straits Times Index (STI) has surged to record highs again – the highest in its entire history. But for investors, the real question is: where do we go from here? And can this growth last?