What I like about Dr Wealth’s courses are that they delve a lot into academic research and market backtesting of strategies before they basically come up with their own formulas which you cannot learn from any investment book outside.

I was recently invited to attend their revamped Factor-Based Investing Course (FBIC) and found it really helpful because whether you’re more inclined towards value investing, dividend or income investing, or trend following (through technical analysis), you’ll learn all of that within this single course.

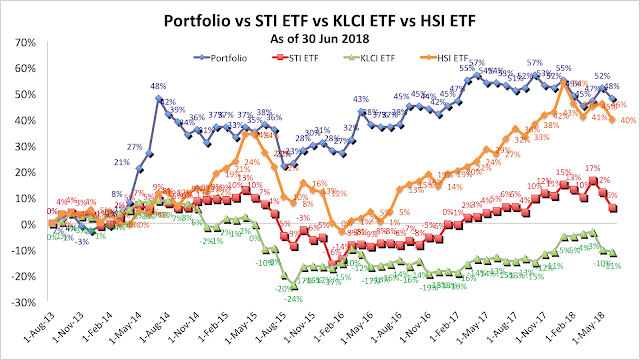

Here’s how their results have been like so far:

What’s their secret?!?!

That was exactly what I wondered, and I found out after attending their course.

As regular readers will know, while I’m a huge advocate of investing in financial education and have attended numerous courses myself, I’m very picky about the ones that I actually recommend, simply because my reputation is on the line.

I also don’t believe in paying a 3 or 4-digit sum just to learn basic concepts like how to save money, how to open a brokerage account, how to calculate P/E P/B NAV or dividend yield, etc, because you can easily learn that online or even from free resources like my blog, SGX, or other financial websites.

As such, I only recommend investment courses that fulfil my following criteria:

- They must be conducted by trainers I personally trust and respect for their investing prowess.

(no, past performance alone doesn’t count. I talk to them and ask them questions to ascertain if this is someone I would listen to when it comes to their take on investments and how sound their strategies are. How much they’ve made or lost is secondary, because investing in the stock market comprises of BOTH luck and skill. Anyone who tells you or claims otherwise is either boasting or lying.) Sometimes this “trainer(s) assessment” process involves me asking them questions on their past (or present) stock picks, and why.

- They must be courses that I’ve personally paid for with my own money, or would be willing to fork out my own cash for (if I was sponsored to attend).

- The price must be value-for-money.

(and I’ll be the judge of that “value”, not them. And no, value does not mean number of hours spent in the classroom but rather, on the quality of content taught.)

- The course must teach something that I cannot find elsewhere in a book, or in any of these books.

This can be either their unique qualitative approach or quantitative formulas. Because if I’m going to spend my time and money learning something that I already know, or which I can learn it for free from NLB or for a fraction of the fee (the book price), then why pay?

- They must be strategies that I agree with and/or use, and would personally advocate on my blog.

Even better if they are strategies I’ve personally adopted into my own investing matrix after attending their course.

- Their investment approach and philosophy to financial literacy and education must be aligned with mine.

As such, there are really only two course providers in the market whom I currently feel confident to put my name behind and recommend publicly – Dr Wealth and The Fifth Person.

- If there’s any up-selling of products or services after the course, it has to be stuff that I also can see the value for, even if I may not sign up for it myself.

Today’s review is on Dr Wealth’s revamped FBIC, and whether it is worth your money…or not.

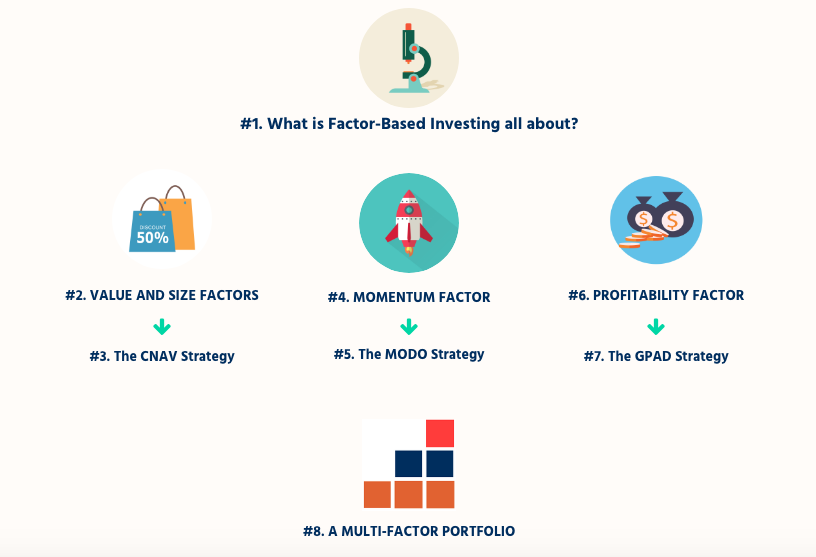

In a nutshell, FBIC consists of four core parts:

1. Conservative Net Asset Value (CNAV) strategy

2. Gross Profitability and Dividend (GPAD) strategy

3. Technical Analysis

4. Portfolio Diversification strategy

CNAV Strategy

Most people are familiar with Net Asset Value, but Dr. Wealth has taken a more conservative approach in the form of CNAV in order to identify stocks where we can pay a very low price for a very high value of assets.

This strategy consists of 2 key metrics and a 3-step qualitative analysis, which I will not divulge here because it is not my intellectual property to share.

Seasoned investors would know that simply taking the book value of a company is problematic, because not all assets are necessarily of the same quality. If you’ve followed my previous stock analysis writings, you’ll also realise that I tend to choose and pick which ones I value and eliminate others which I don’t really care for. Dr. Wealth follows the same method, although they’ve simplified it into a qualitative step-by-step formula for people to apply.

There are many stocks trading at low multiples of their book value on SGX, but does that make them undervalued? Obviously not! Many of them could in fact be value traps i.e. cheap due to their poor fundamentals.

Knowing what are the right metrics and qualitative factors to apply would be the key to your investing success in filtering out the cheap and bad goods from the undervalued gems.

The CNAV strategy tends to favour certain stocks due to its focus on particular asset qualities. As such, growth stocks like FANG (Facebook, Amazon, Netflix, Google) would completely fail the criteria because they do not hold much assets in that sense.

As such, this is where the GPAD strategy comes in to help one identify asset-light businesses that have competitive advantages over other companies and whose profitability has been proven sustainable.

Suitable for investors who seek dividend-paying stocks while looking for potential capital gains, I’ve found this GPAD strategy helpful in honing my investment method (which is a variation of GPAD as I find its rigour too time-consuming for my regular investment research, given my limited time since I work and also blog!).

In other words, wanna get paid while you wait for capital gains? GPAD strategy might just be your answer to identifying those gems.

In recent years, there has been more investors (and bloggers) who adopt a “fundamental momentum strategy”, which basically entails the combination of strong fundamentals riding on a strong momentum.

This increases the possibility of one profiting, in contrast to simply focusing on fundamentally strong and undervalued stocks which could remain undervalued for a long time. I know, because I own two stocks in my portfolio which I think have been grossly undervalued since I first bought them in 2015 and I still cannot understand why the market has been so blind to their value. All my calculations and attempts to prove my own thesis (that they’re massively undervalued) wrong have failed.

Since traders rely more on momentum, it looks at prices alone without the need to analyse the fundamentals of the underlying businesses. This is where technical analysis comes in to determine one’s entry and exit signals. Dr. Wealth advocates methods like price action analysis, in contrast to the Moving Average (which most TA folks use), as they believe the former enables an investor to join in and ride a trend more easily.

I’m not a big fan of TA, but I’ll admit that I do look to them sometimes to determine my entry and exit points when I’m applying my fundamental momentum strategy because it is a stock that I believe in only for the mid-term. For cryptocurrencies, TA becomes all the more important and I combine it with fundamental analysis in order to decide whether to buy or sell a crypto now, or wait.

You can learn the differences between the TA indicators and hear from an experienced trader, Alex, within Dr. Wealth’s team, and decide which ones you wish to adopt for yourself.

Portfolio Diversification Strategy

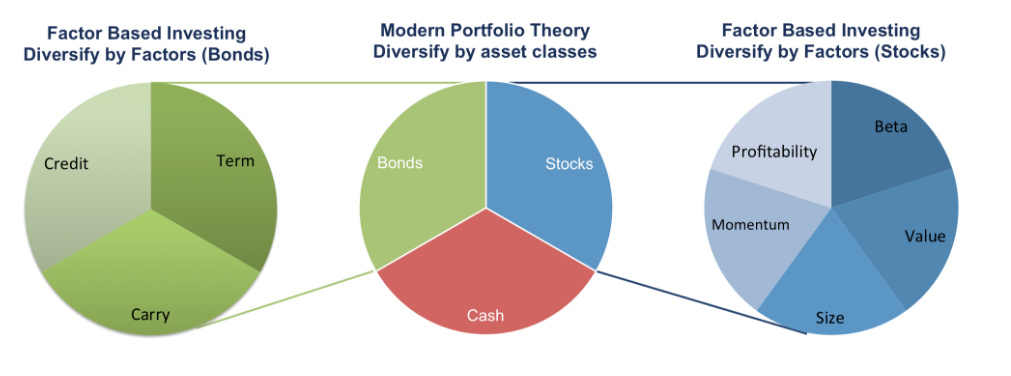

There are many ways you can diversify in order to minimise your risks – across multiple stocks, different industries, various stock markets, or even just varying investment asset classes.

Backtesting has shown that diversifying by factors actually perform better than simply diversifying across a large number of stocks. In fact, I’m also not a fan of having too many stocks in one’s portfolio, because time now becomes the limiting factor – do you have enough time to monitor the developments in all these stocks?

I know I certainly don’t. Some investors prefer to keep their portfolio within 20 stocks, others prefer 10, while I even know of a few who have their entire capital confined to just 3 – 4 stocks!

In FBIC, Dr. Wealth teaches their own portfolio diversification strategy and how it has enabled them to consistently achieve superior returns. This is crucial because we need to also remember that as much as you’re gonna have great winners, you might have some losers too (due to luck!) and without proper portfolio management, this can really skew your returns.

The course lasts 2.5 days and will be divided according to the following:

– Day 1: How to detect stocks with size and value factor advantages using CNAV strategy

– Day 2: How to pick stocks with the profitability factor using GPAD strategy

– Day 3 (3 hours): How to identify and grab investing opportunities

That way, you’ll be able to suss out the trainers and decide for yourself if their content is worth finding out more on, instead of just taking my word for it.

And would I recommend it?

Having been through the course myself and currently applying some of their strategies to my own portfolio, my answer is a resounding yes. I’ve attended many investment courses / previews in Singapore, but you don’t find me talking about many of them here because I’m always so turned off / never feel like the price is quite worth what I learnt, so you can be rest assured that if you see my review here, it means I see enough value in it to put my name behind them.

Check out the class preview dates here if you’re keen to find out more, and let them know you’re a Budget Babe reader if you do go!

Open disclosure: I was invited to attend their course but was not paid nor expected to write a review. My opinion and review remains fully unbiased and objective – I’ve attended others and found them so bad that I don’t even write a single word about them – but in case you should need more unbiased reviews from other customers who paid for their own course, you can find those reviews here.

As regular readers who have been following my blog for a few years would know by now, I only review and recommend stuff I truly find value in, and FBIC stands out in contrast to the many other investment courses out there for their quantitative metrics and approach to deep value investing. If you don’t see me raving about a course provider on my blog, then I’m not recommending it / not a fan, full stop.

With love,

Budget Babe

19 comments

A very objective review, will check them out!

I have been a silent reader of your blog because I like some of your past articles which talks about how to buy stuff with a tight budget. However, I disagree with this post. I have friends and relatives who have bad experience with financial training courses that charge around $1000 for a 3-day course. How can a course be value-for-money when they charge several hundreds for a few days course when the materials can be obtained free of charge from libraries and advice easily sought on online forums? You may be missing out on good investment books if you cannot find some of the materials in the course in books. The CNAV concepts were introduced in books like "The Intelligent Investor" (written > 50 years ago) by Benjamin Graham and "Your First Million" written by the late Dr Michael Leong. "What works on Wall Street" by James P. O'Shaughnessy and "Your Complete Guide to Factor-Based Investing" by Andrew Berkin/Larry Swedroe are good books on factor-based investing. I have not attended the course that you reviewed. I trust your judgment that the material is good quality based on the past articles you wrote. Even if the training material is good quality, does it beat buying the right books and re-reading them to digest the materials slowly instead of trying to absorb them in a few days and paying close to $1000?

When writing reviews, I will trust reviews when it is written with 100% disclosure about whether the writer makes money from it. While you may not be paid to write the review directly, may I ask are you paid in other ways? Do you get paid when your readers use the "BBSPECIAL" to sign on the investment course that you reviewed? Having said that, it is absolutely ok for bloggers like you to make money from writing blog articles since nobody works for free. I will do the same thing if I were in your shoes but full disclosure is recommended to preserve one's reputation built up over time.

I have to agree with Lita. The CNAV principles were similar concepts written in "The Intelligent Investor" by Benjamin Graham. The people at Dr Wealth or the old BFP actually made very minor modifications to it (by adding investment properties etc) and claim they came out with the formula. In fact, if you read Security Analysis, Graham himself alluded to adding investment properties and the like to complement his net working capital formula. I find it extremely distasteful to claim the formula their own when obviously 95% of the work is done by Graham himself. The same can be said about the so-called GPAD formula – found in many articles or books but only small minor modifications were made. Such formula may or may not work but please give credit where credit is due.

I would like to end this by highlighting that there are many stocks in SGX or in other markets that fits CNAV and/or GPAD criteria. Selectively using just a few stocks or a single portfolio (where the stocks and trades were never revealed at the beginning and at times, even at the end) that met this requirement and showing them having seen huge rises in the stock prices over a short period of time can be very misleading. Like stock picking, the buyers of any investment courses have to make rational judgement based on alternatives, quality and price before making any commitments.

Hi Lita,

Thanks for letting me know! I've read The Intelligent Investor as well as Your First Million, but not the other two you've mentioned, so I'm not familiar with whether their formulas are inside those books, but it isn't for the first two. You're wrong about it being in the Intelligent Investor though, because what Alvin Chow and his folks have done is to modify Graham's strategy of net asset value. CNAV =/= NAV nor the margin of safety that Graham preaches about, but instead, it is a modification of the strategy which Dr Wealth has made.

Of course, if it is indeed found in its exact form in other books, please enlighten me and I will make the necessary modifications to this post!

You asked if the training material beats buying the right books and re-reading them to digest the materials – I've mentioned this before and have not changed my stance: if one does not have the money but has the time and discipline, books will always be the best and cheapest method to learn. I've even written and consolidated a list of my favourite books and have referred many readers to this post endlessly during every single talk that I've given: https://www.sgbudgetbabe.com/2017/07/recommended-books-on-personal-finance.html

However, books shouldn't be compared in the exact same vein as investment courses. To me, (the right) investment courses offer more value that books alone cannot – you learn more in a shorter period of time (like a crash course), you get to ask questions to the trainers that you can't ask the book authors all the time, it is more interactive with hands on practice, and you get to hear from the course instructors on their mistakes / common misinterpretations of the strategy or strategies. These cannot be found in books, and for someone who is time-pressed or takes a really long time to read / learn better from a face-to-face interactive course, they might find investment courses better for their learning progress.

it is akin to comparing tuition and school textbooks. why then should anyone pay for tuition since you can "buy the right books and re-read them to digest the materials slowly"? but yet crash courses for A Levels / O Levels / PSLE prep still thrive. It simply is a better of personal preference.

Also, disclosure has been provided at the end of the blog post, which you can read as per my usual policy (under Collaborate!).

Thanks for the feedback! I await to hear from you as to whether I'm wrong on CNAV and the other strategies not being in the other books – if it is indeed the case, I will be making the right edits as I don't want to be spreading wrong or misinformation!

Cheers,

Dawn

Hi Chris!

Thanks for letting me know that! I will be checking with the folks at Dr Wealth to see if any of the information in this article which I've written is actually false / misleading like you've claimed, and will be making the necessary changes if that's indeed the case as I do not want to be spreading misinformation.

I've read The Intelligent Investor, and CNAV is a modified version of what Graham preaches, but it is not the exact same that was purported in the book. I've not yet read Security Analysis though, but it is on my list, so I'm not familiar with Graham's allusion to adding investment properties to complement his net working capital formula, but thanks for letting me know! I'll be checking with the folks at Dr Wealth right now 🙂

Many thanks,

Dawn

Btw adding on, BBSPECIAL is not the only code readers can use to get the discounted price – there are plenty of ways one can get it for <$1000 and not full-price (a reader of mine actually signed up prior to my review being published and also paid the same without my promo code, which wasn't ready then). in fact, I was the one who asked for a customized promo code that I could share with my readers instead of their usual generic ones!

hope that clarifies!

they have a free 2.5 preview if you'll like to visit them first to check it out before committing anything / any money! I highly recommend that for anyone who's interested in considering whether this will be worth your time and money.

Hi Lita, sorry to hear that your relatives have bad experiences with investment courses.

Maybe you are someone with good intelligence and could digest information quickly and put them to action. Most people do not and that is why even though all the information is in the internet for free, libraries are full of free books to borrow, we still spend most of our adolescent years to school. To learn and ask questions. To practise and think.

If information is accessible to all, why do we have inequality in society? Hence there are some people who needs to have a proper environment to learn. I think we have to respect and give people chances who have lesser ability than you.

This comment has been removed by the author.

Hi Chris, maybe you have attended our courses before or maybe you have not. We have never claim any proprietary strategies. We also acknowledge Graham for value investing, and also Fama and French for Factors. We also acknowledge Robert Novy-Marx for Profitability Factor.

Because we have made adjustments to the strategies we have to give it a different name, lest people say we abuse the methods mentioned by those greats.

You can see the numerous quotes in our write up here: https://www.drwealth.com/factor-based-investing/

The portfolio returns is based on an actual real stocks portfolio which we practise what we have taught. You are right that performance will differ from person to person but there's no better way than putting our money where our mouth is.

And just to add, I produce a lot of material about investing online for free. If people can grasp what I am saying then they wouldn't need to come for the course. We are truly sincere about teaching.

I have done a book review on the Factors book by Larry Swedroe:

https://www.drwealth.com/your-complete-guide-to-factor-based-investing/

Graham's net net strategy explainer (i dont change the name of the strategy if i dont modify it)

https://www.drwealth.com/warren-buffett-strategy/

Here's a detailed write up about Factors.

https://www.drwealth.com/your-complete-guide-to-factor-based-investing/

Hi Dawn,

Thank you taking the time to reply.

Managing one's hard-earned savings, accumulated over a lifetime, is a life-critical activity. If managed badly, the person's life is screwed. Would any of us feel safe to have our money managed by a fund manager who says he is too time-pressed and cannot afford the time to "read books, re-read good books and digest them slowly" and prefers to take "short-cuts" like attending short 2.5 days course instead? Would any of us be comfortable to have our money be managed by a fund manager who is not willing to take the far longer but more thorough process of learning through books and internet resources on his own? Yet, many of the students who took up expensive 3-day trading/investment courses are like this fund manager. These students see mainly the financial freedom which was skillfully sold to them by the financial trainers but do not appreciate the necessary sacrifice in time and effort involved in actively managing their own money. If these students are willing to endure the longer process of learning through books and internet resources which are freely available, then it is not a value-for-money choice to attend 3-day courses that charge close to $1000, particularly if they do not have a lot of money to spare.

For people who simply do not have the time nor discipline to personally manage their own money, it is not necessary to do it on their own. They can outsource money management to cheap passive index funds or even the more expensive professional active fund managers. Both options are better than "fund managers" who are not willing or unable to put in the time.

Face-to-face interaction is certainly a plus. Such to-and-fro interaction is also available freely on the internet free of charge. Interaction from experienced and sincere investors is freely available at online forums today and the Q&A session last forever as long as the thread is alive.

I did not attend the CNAV course. However, I am sure the CNAV strategy is not found in its exact form in other books. Mr Alvin Chow sounds like a decent guy and should be smart enough not to plagiarise from other sources without modifications and sell as his own. In fact, the experienced investors that I know make modifications of their own to whatever they have learnt from books, interaction from fellow investors and losing to Mr Market. I do not know of experienced players who take other people's strategies without their own modifications to suit their own unique situation and psychology.

It is one thing to pay for expensive tuition and crash courses to game the exam systems like A Levels / O Levels / PSLE. The student and teacher care mainly about scoring good grades. It is totally a different thing when it comes to life-critical activity like managing your wealth. If one has no time and not enough discipline and passion, please let the professionals or preferably, the cheaper and better-performing passive funds handle your money. Don't DIY. And if a person wants to DIY, please don't take short-cuts and be prepared to take the pain. Don't get intoxicated by the siren song of Financial Freedom and lose sight of the sacrifice involved.

Hi Alvin,

I have read some of your past articles on your blog, both BigFatPurse and DrWealth. In fact, I very much prefer the old articles on BigFatPurse which I sense were more sincere because it was not biased by the need to make money like DrWealth. When money came into the picture, there was more hidden agenda behind the articles. Are they marketing materials for the more expensive courses? This is inevitable since you have to earn a living. I understand the position you are in. We readers have to be more discerning when reading articles by bloggers who depend on their blogs fully/partially for a living since nobody works free of charge.

Among the financial trainers in the industry, I sincerely compliment you as among the more decent and less aggressive ones. You are definitely superior to financial trainers like Clemen Chiang who got sued for his options-trading course.

http://www.singaporelaw.sg/sglaw/laws-of-singapore/case-law/free-law/high-court-judgments/14070-freely-pte-ltd-v-ong-kaili-and-others-2010-sghc-60

Although I have not attended your course, I believe the content to be of good quality based on your past articles. Having said that, I do not find your value investing course to be value-for-money since it charges close to $1000 for a 2.5 day course when similar (not exact, of course) materials can be found in books and discussed on internet forums which can be accessed free of charge.

Thanks Lita for your compliment.

I guess you do not value investment courses. It is totally understandable that we value things differently in our lives.

For e.g. I don't value physical coaches as I believe I can do my own exercises. You don't value investment trainers because you can do it by yourself.

And based on your reply is that people who are not determined to figure out by themselves by reading (and not attending courses) are not worthy enough to DIY their investments. I think having the motivation to learn even through courses should be applauded and not throw wet blanket on them. Maybe it is an Asian culture that we tend to look at the cup half filled, and point out the negative things rather than encourage with the positive.

I want to draw parallels to other kinds of courses.

I have been sent for corporate training in the past whereby the organisation paid thousands of dollars for a few days course. I didn't apply anything I have learned in my work and I think some people can resonate with that. But we will go again because we didn't pay for it. It is 'free'. Someone paid for it doesn't make it free.

Universities also provide continuous learning and charge thousands of dollars but people find it worthwhile because they have a name. It is ok to pay money for it. The attendees don't complain the materials are taught online for free.

Some people may buy a 20k Patek Phillippe and feel that it's worth it.

Some poeple pay 10k to travel around Europe and it's worth it.

Some people pay 1m for a Ferrari and it's worth it.

Personally I have paid for investment and other personal development courses and I have never regretted even when they cost much more than what I charge for my courses. I saved a lot of time straightening my thoughts. I find that perspective shifts the most rewarding and I would gladly paid for it. If I can reach my goals faster, I would pay for it. Time I cannot buy.

A course is not a short cut. We have never said that. It just give people a start. I wouldn't be where I am today if I had not attend courses and of course, read books as well.

Your path to success is one way but there are many roads to Rome. Who are we to judge our path is the best? Let the people figure out their ways.

Hi Lita!

I agree and as you've said so yourself, "If these students are willing to endure the longer process of learning through books and internet resources which are freely available, then it is not a value-for-money choice to attend 3-day courses that charge close to $1000, particularly if they do not have a lot of money to spare."

However I don't think we should throw wet water at those who may find that courses could offer better value to them than books, as well as teach more in a shorter period of time.

I'm largely for self-learning through books, but as a teacher, I've also seen how this method is not one that every student is suited to. Some misunderstand what is being taught in books, and if applied wrongly to real capital markets, their "tuition fee" paid to Mr Market could end up being wayyyyyy more than what they could have paid for to avoid the same mistake through an investment course.

I'm a huge advocate of books, and I used to not believe in investment courses either. However, after attending many myself, I've realised that courses have helped me as well and I don't regret paying for the ones that offered real quality. While I did not pay for FBIC as I was sponsored to attend, I would willingly pay the $1k for it because it'll take me more than 2.5 days to learn and pick up what Dr Wealth taught. To me, I value my time at more than $1000 so it makes it worth it.

But you're right – someone with little money / capital but all the time in the world would be better off reading books, practising and paying Mr Market tuition fees instead. There are different learning methods for everyone.

You sound like a smart and experienced investor and so it seems FBIC (and maybe every course out there) would not be the best fit for you. But that's not to say it may not be a good fit for others 🙂

Hi Alvin,

Certainly, people should figure out themselves on whether a 2.5 days course costing close to $1000 is suitable for them. It is not a technical question with a clear right or wrong answer because everyone's situation is different.

The problem is the way such courses are being sold to them by the financial trainers. An effective way to sell expensive financial courses is by singing the siren song of financial freedom, poking at how hateful a day job can be, how wonderful early retirement can be, YOLO, playing on their psychological weaknesses/desires and finally how their courses can help them achieve financial freedom. Of course, no financial course in the world can promise financial freedom. This is a claim that an irresponsible, unscrupulous financial salesmen will make because when they know nothing serious will happen to them if the claim is not fulfilled.

Here are some legitimate questions the students should ask.

1) since the financial trainers imply that the courses will help the students achieve financial freedom, have the trainers reach financial freedom themselves? If no, the trainers may be trying to teach their way to financial freedom.

2) if the financial trainers have reached financial freedom, how did they do it? Is it through investing/trading their own methods which they are going to teach, or is it through teaching their financial courses by collecting fees from the students?

If the students are too polite to ask, they can do a simple observation test. Do the trainers look young? Young people lack the time to compound their wealth to reach financial freedom.

3) When financial trainers sell an investment strategy and claims that it has X returns in Y years, the students should ask for documents that show the past trading transactions to do the verification for themselves. It is not a good sign if the financial trainers refuse to produce data that allow students to verify on claims made.

Among the friends and relatives who can afford to buy 20k Patek Phillippe, $10k to travel around Europe, $1m for a Ferrari and find them worth it, I am not concerned even if they want to pay $10k for a 1-day investment course. Dawn feels that 2.5 days of her time is worth more than $1000. She belongs to this privileged group. Unfortunately, many people going for the expensive investment/trading/financial-freedom courses do not belong to this privileged group and are vulnerable to financial sellers who prey on their psychological weaknesses. In fact, the lesser money they have, the more vulnerable they are in falling for the financial freedom sales talk.

Good for you that you have good experience from investment/trading courses. There is no guarantee that students taking on expensive courses can get good experience like you. What is guaranteed is the high price they are going to pay. Financial salesmen like to say you got to pay high prices to get good quality stuff to get their clients to buy high-priced products that help the salesmen earn high commission. Those who are savvy about financial products know high prices do not always mean high quality in the financial world. Think of active unit trusts versus passive index funds/ETFs, investment-linked insurance products/whole life versus term insurance. The high costs feed the financial salesmen who sell the products.

Hi Alvin,

My path to success is one way and there are many roads to Rome, as you said. Certainly so and my self-learning way through books and internet resources may not be favoured by others. Rightly so. My intention is not to be a wet blanket. I am providing perspective from the other side to counter the perspective offered by biased financial salesmen. Biased salesmen will emphasize the positive side for self-serving reasons, so discerning customers must see the negative side for themselves to make an informed decision. Nothing to do with Asian culture of seeing the cup half-filled, and point out negative rather than encourage the positive. In fact, if a value investor has a tendency to be biased towards the positive and ignore the negative, he had better not invest his money.

The value of online sites such as this blog is that it allows people with different perspective who disagree with each other to have a discussion. Both of us disagree and our discussion here will allow readers to understand both sides of the coin to make a more informed decision. I believe the comments section has added value to Dawn's blog readers.

Hi Dawn,

I don't find the course a good fit for me but I'm sure it is a good fit for you based on what I am reading. It is a judgment each of us make based on our personal situation. For example, you value your time at more than $1000. Naturally, it is a good fit for you.

The concern that drove me to make the comments here is that those with little money/capital tend to be vulnerable to the financial freedom sales talk sung by the financial salesmen. By posting here, your readers will get to read both sides of the issue so that they can make a better informed decision. Your readers are more likely to be happier with the outcome of their decision if they make decisions after seeing both sides of the issue.

Just to clarify in case you like to lump us with the rest of the aspirational selling Trainers.

We always have to differentiate ourselves or even disassociate with them.

To address your points, we never sell ppl the idea of financial freedom or early retirement except Chris Ng’s course because that was his goal and he has achieved it through aggressive savings and dividend stocks.

For factor based investing we just want to prove that there’s a scientific way to achieve higher investment returns. And I have all the trade records to back up the above performance. Ppl can come to my office to verify if they want.

One can also read the reviews by our graduates on seedly: https://seedly.sg/reviews/investment-courses/dr-wealth#reviews

And lastly, investment requires capital. It is not about being privileged or not. If one doesn’t have capital he should not even invest, and definitely not attend a course.

And yes, agree to disagree. it’s good to have open discussion and let the readers discern for themselves.

Comments are closed.